An extreme like that forces a question with no neutral answer: is this the discount of the cycle, or evidence the digital gold thesis is breaking? Right now the market is answering it three d

An extreme like that forces a question with no neutral answer: is this the discount of the cycle, or evidence the digital gold thesis is breaking? Right now the market is answering it three different ways at once.

Key Takeaways

- The BTC/gold oscillator hit its most oversold level ever recorded; the prior flash preceded a ~660% rally.

- Polymarket bettors give Bitcoin just 13% odds of beating gold and the S&P 500 in 2026.

- Cathie Wood expects the ratio to reverse both ways: Bitcoin up, gold down.

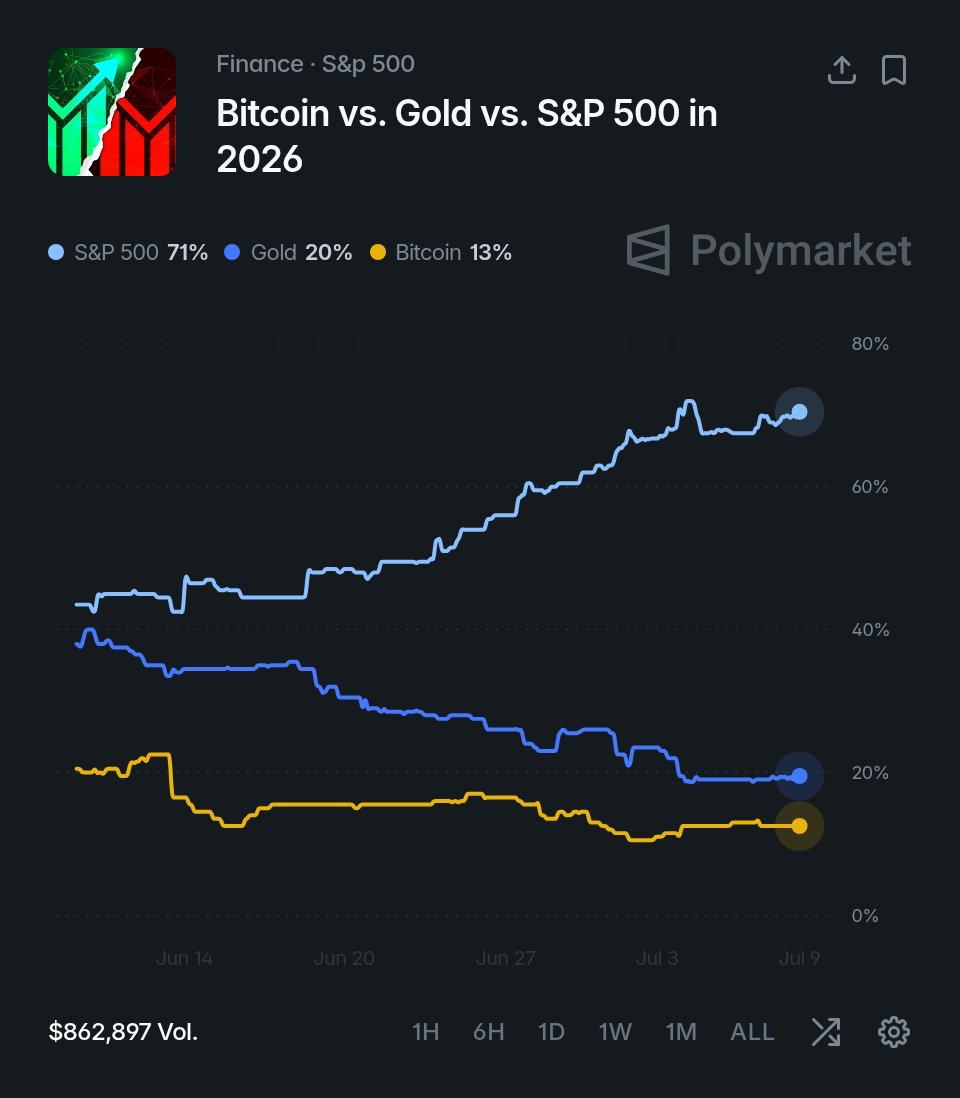

What the Crowd Is Betting

On Polymarket, traders wagering real money on 2026’s best-performing asset give the S&P 500 a 71% chance, gold 20%, and Bitcoin just 13%. The trend is as telling as the level: Bitcoin’s odds have drifted down from around 20% in mid-June while the S&P’s climbed from the mid-40s, meaning the crowd has spent a month growing more confident that Bitcoin finishes last among the three.

Comparative performance chart of the S&P 500, Gold, and Bitcoin as of July 9, 2026.

One caveat belongs next to any prediction-market number. These figures are a betting reflection of public opinion, shaped by the traders on the platform, and they do not necessarily track the objective financial reality of the assets. Prediction markets can be volatile, and prices can be moved by a small number of well-capitalized traders or even attempts at manipulation. What the 13% honestly measures is sentiment among people willing to stake money on it, and that sentiment is firmly against Bitcoin.

What the Contrarians See in the Same Number

The case for the other side starts with the oscillator itself. The only comparable oversold flash in the indicator’s history was followed by a rally of nearly 660% over the following years according to post from Cointelegraph, and the monthly version of the chart sits at its second-most oversold reading ever.

Mean-reversion logic says the moment a ratio is stretched furthest from trend is precisely when betting on its continuation is most dangerous, and 13% odds on an asset at a record statistical discount is the kind of setup contrarians collect.

Cathie Wood made the argument explicit this week. Presenting ARK’s Bitcoin-to-gold chart, she noted the ratio is holding above its last two major lows despite the pressure on Bitcoin and gold’s simultaneous surge, and framed the reversal as coming from both directions: “we expect Bitcoin to gold to turn around,” with the Bitcoin price rising and the gold price falling.

ARK’s framing ties the call to its larger thesis that Bitcoin is the core of a new global monetary system, which is worth knowing when weighing the prediction: the firm is structurally long the outcome it forecasts.

The contrarian read also lines up with positioning data covered in recent cycle analysis: capital rotated from Bitcoin ETFs into the AI trade through the spring, half of holders sit underwater, and sentiment gauges are at yearly lows. Extremes in price, odds, and mood arriving together is what capitulation zones have historically looked like.

READ MORE:

Clarity Act’s 2026 Window Could be Closing: Here’s Why

Clarity Act’s 2026 Window Could be Closing: Here’s WhyThe Bear Who Rejects the Question

Peter Schiff, gold’s most reliable advocate, dismisses the entire framework. Bitcoin was never really correlated to gold despite the digital gold branding, he argued this week, and the correlation that did exist, with the Nasdaq, has broken down in the worst possible way. Bitcoin no longer rises when the Nasdaq rises, he wrote, “but I think it will still fall when the NASDAQ falls.”

Strip out the polemics and Schiff’s point is the sharpest version of the bear case: an oversold ratio only mean-reverts if the two assets genuinely belong in the same category. If institutional money has permanently filed gold under monetary hedge and Bitcoin under risk asset, the ratio can stay stretched or keep stretching, and the oscillator’s historical precedent, built mostly on years when Bitcoin traded as an emerging monetary asset, stops applying. The 660% rally that followed the last flash is a sample size of roughly one.

That is the real dividing line under all three camps. The BTC/gold ratio is no longer just a valuation signal; it has become a classification test. Polymarket traders are treating Bitcoin like a lagging risk asset, Cathie Wood sees a suppressed monetary asset, and Peter Schiff rejects the comparison entirely.

At minus 1.81 sigma, the ratio does not settle the argument. It only raises the cost of being wrong. A rebound from this extreme would support the mean-reversion case and suggest Bitcoin was temporarily mispriced against gold during a macro and AI-driven rotation. A continued decline would send a harder message: the market is no longer willing to grade Bitcoin as digital gold.

The data does not prove the thesis has failed, but it does show that Bitcoin no longer gets the comparison for free. It has to earn it back through relative strength against gold, not through narrative alone.

The information provided in this article is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Cryptocurrency markets are volatile and involve substantial risk. Readers should conduct their own research and consult with a qualified financial advisor before making any investment decisions.

The post Bitcoin vs. Gold: Is the “Digital Gold” Thesis Breaking? appeared first on Coindoo.