Fed stablecoin policy is entering a broader phase as the Federal Reserve examines how dollar-backed digital assets could influence cross-border capital movement, safe-asset demand, bank fundi

Fed stablecoin policy is entering a broader phase as the Federal Reserve examines how dollar-backed digital assets could influence cross-border capital movement, safe-asset demand, bank funding, and the future structure of the global dollar system. Federal Reserve Governor Christopher Waller placed stablecoins inside the central bank’s dollar research agenda during the Fifth Conference on the International Roles of the U.S. Dollar held on June 22, 2026.

The discussion marks a shift in how policymakers view stablecoins. They remain crypto trading tools, payment tokens, and regulatory objects, but they are increasingly being studied as a private layer built on top of public dollar infrastructure. The issue is not only about digital payments.

Stablecoins can create new channels through which global users access dollar-denominated assets, while their reserve portfolios can connect them with banks, money markets, and short-term U.S. government securities. The Federal Reserve’s focus is centered on understanding whether stablecoin growth will mainly expand global dollar access or create new pressures through bank deposit changes, liquidity risks, and market structure shifts.

What does Fed stablecoin policy mean for the future of dollar infrastructure?

Fed stablecoin policy refers to the Federal Reserve’s examination of how stablecoins interact with the wider dollar economy. The focus has expanded from crypto markets to questions involving international payments, reserve assets, financial intermediation, and dollar liquidity. During the June 22 conference, Waller said distributed ledger technologies and tokenized assets such as stablecoins are creating new channels for global dollar intermediation.

Fed Stablecoin Policy Shifts as Waller Puts Stablecoins on Dollar Research Agenda

These channels can operate alongside traditional banking and payment systems. The conference was organized around the changing international role of the U.S. dollar and examined how digital assets could affect investment flows, payment networks, market structures, and reserve currency dynamics. Waller said the traditional foundations of dollar strength remain important, including the size of the U.S. economy, the depth of financial markets, institutional trust, and the rule of law.

At the same time, he noted that technology is changing how people and businesses interact with dollars. “The private sector is moving rapidly to expand access to dollar-denominated assets, innovate in new financial services, and explore potential business opportunities that perhaps did not make sense with legacy technologies,” Waller said.

Stablecoins started as crypto trading tools, but their wider use has turned them into a bigger policy issue. A dollar-backed stablecoin gives users a way to hold and send digital dollars through blockchain networks including across borders. For policymakers the key question is how these private digital dollar channels interact with the existing financial system. Stablecoins may expand access to dollar assets for users outside the United States.

They may also influence how dollars flow into reserve portfolios, short-term securities, and banking channels. The impact depends on where demand comes from. Offshore users seeking digital dollar access may create a different effect compared with domestic users moving money away from bank deposits. This distinction is central to the Federal Reserve’s research because stablecoins could either complement existing financial systems or compete with parts of them.

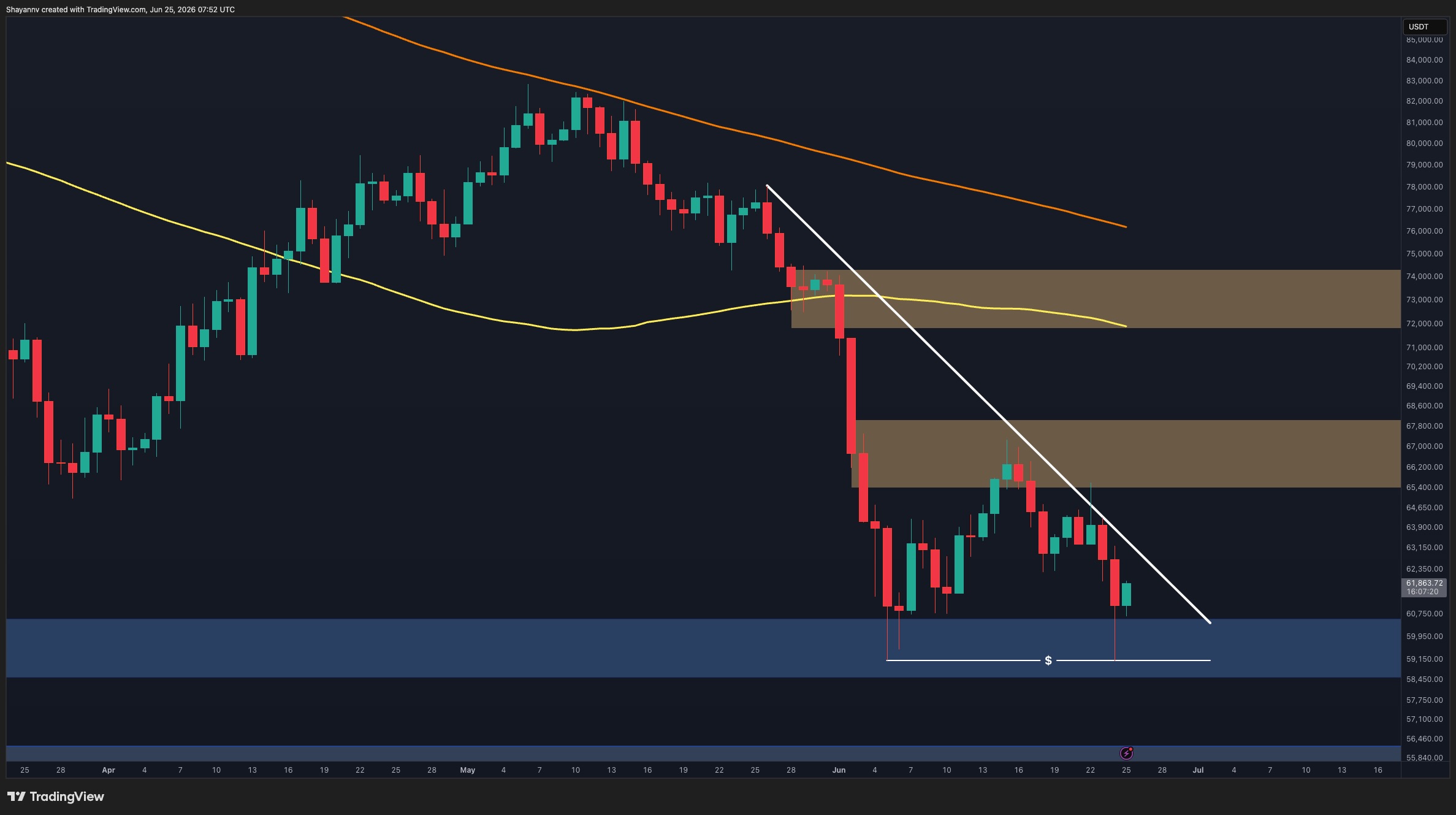

How large is the stablecoin market and why does scale matter?

Stablecoins remain small compared with the full size of global financial markets, but their scale within crypto has become significant. Data showed Tether and USDC among the five largest crypto assets by market capitalization on June 25. USDT had a market capitalization of nearly $186 billion, while USDC stood at nearly $73.8 billion.

Tether’s 24-hour trading volume was around $81 billion, compared with Bitcoin’s roughly $43 billion during the same market view. These figures have increased attention on how stablecoin issuers manage reserves and handle periods of rapid growth or stress. Circle’s own materials showed USDC circulation at $74.3 billion as of June 22. Circle described USDC as backed by highly liquid cash and cash-equivalent assets.

Circle also stated that most USDC reserves are held in the Circle Reserve Fund, an SEC-registered government money market fund managed by BlackRock. These reserve arrangements are important because stablecoin growth can influence demand for short-term dollar assets. Increased demand may support markets at the margin, while sudden redemptions could create pressure during periods of market stress.

How could stablecoins affect banks, Treasury bills, and liquidity markets?

Stablecoins connect digital asset markets with traditional financial structures through their reserves and payment activity. A rise in stablecoin demand could affect bank deposits, money market funds, repo markets, and Treasury bills depending on how issuers hold backing assets. The Federal Reserve is studying whether stablecoins could change bank funding conditions.

The impact could vary based on whether growth comes from new offshore dollar demand or from users replacing traditional bank balances. Stablecoins are also being examined for their possible impact on safe-asset demand. A June BIS working paper found that dollar-backed stablecoin inflows can lower short-term Treasury bill yields, with stronger effects during Treasury market stress and as the sector grows.

The finding focuses on shorter-term securities and does not suggest stablecoins determine the entire Treasury market. Treasury advisory materials provide additional context. A 2026 Treasury Borrowing Advisory Committee presentation found that major stablecoin issuers hold less than 1% of outstanding Treasuries. The presentation also noted that future stablecoin expansion could increase demand for short-end Treasury issuance if growth is driven by offshore users seeking dollar exposure.

What response are banks and regulators preparing?

The growth of stablecoins has encouraged banks to explore their own digital settlement systems while regulators continue studying possible risks. The Clearing House announced on June 5 that major financial institutions are supporting an on-chain commercial-bank-money initiative. The project aims to support tokenized deposit clearing and settlement while connecting blockchain activity with RTP and CHIPS.

Fed Stablecoin Policy Shifts as Waller Puts Stablecoins on Dollar Research Agenda

The move highlights a wider competition between privately issued stablecoins and regulated forms of digital banking money. Regulators are also watching risks related to reserve concentration, redemption pressure, liquidity shocks, and monetary policy transmission.

Stablecoins may improve payment efficiency and broaden access to dollar assets. However, greater integration with financial markets means problems in stablecoin markets could have wider effects. The Federal Reserve’s approach remains focused on research and understanding rather than adopting a specific stablecoin model.

Conclusion

Fed stablecoin policy shows that stablecoins have moved from a crypto-focused discussion into a broader debate about the future of dollar infrastructure. The Federal Reserve is examining stablecoins as both a possible extension of global dollar access and a potential source of new financial system challenges. Their growth could support cross-border payments, increase demand for dollar-linked assets, and create new financial services.

At the same time, policymakers are studying how reserve management, redemptions, bank funding, and Treasury-market effects could influence stability. The next stage will depend on how stablecoin adoption develops and how effectively the financial system absorbs these new private dollar channels.

Glossary

Fed Stablecoin Policy: The Fed’s study of stablecoins and the dollar.

Christopher Waller: Fed Governor focused on stablecoin research.

Dollar Liquidity: The flow and availability of U.S. dollars.

Bank Funding: Money banks use to operate and lend.

Treasury Bills (T-Bills): Short-term U.S. government debt.

Frequently Asked Questions About Fed Stablecoin Policy

Why is the Federal Reserve studying stablecoins?

The Federal Reserve is studying stablecoins because they could change payments, bank funding, and dollar liquidity.

Why are stablecoins important to the Fed?

Stablecoins may affect banks, financial markets, and how people around the world use U.S. dollars.

Can stablecoins affect bank deposits?

Yes. Some people may move money from bank accounts into stablecoins, which could affect bank deposits.

Which stablecoins are the largest?

USDT and USDC are among the largest dollar-backed stablecoins by market value.

How do stablecoins support global payments?

Stablecoins can help people send and receive digital dollars quickly across borders.

Sources

Federalreserve

Cryptoslate

Federalreserve

Lexology