Key Takeaways Hyperliquid surpassed $1.2 billion in cumulative trading fees by July 10, 2026, according to Grayscale data sourced from Allium. A portion of protocol fees is automatically conv

Key Takeaways

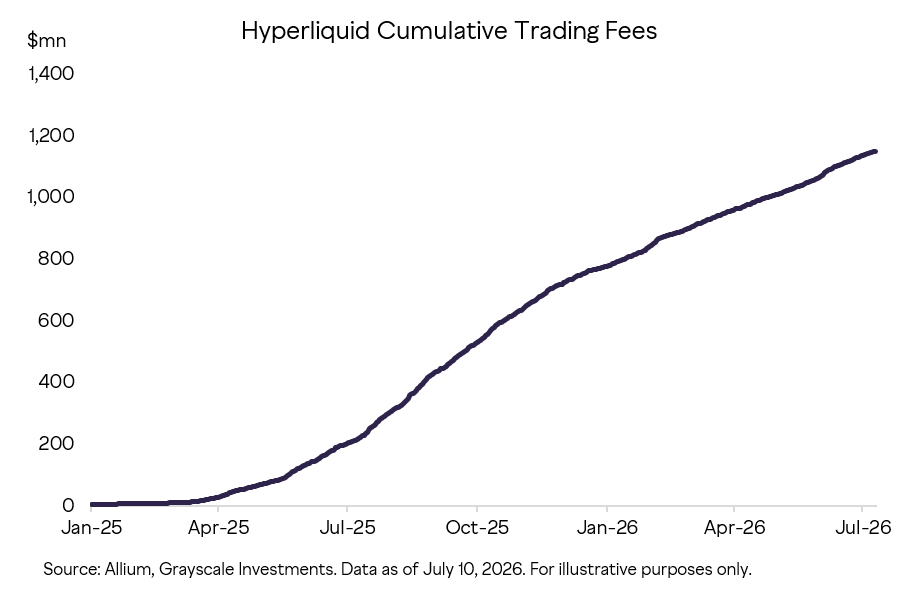

- Hyperliquid surpassed $1.2 billion in cumulative trading fees by July 10, 2026, according to Grayscale data sourced from Allium.

- A portion of protocol fees is automatically converted into HYPE, and the acquired tokens are burned, linking trading activity to token demand and supply reduction.

- HIP-3 and builder codes allow outside teams to launch markets and earn revenue without creating a separate trading stack.

- Grayscale already offers direct HYPE exposure through its Nasdaq-listed Hyperliquid Staking ETF, HYPG.

- Regulatory progress supports perpetual futures as a product category, but it does not remove Hyperliquid’s U.S. restrictions or operational risks.

Grayscale’s Head of Research, Zach Pandl, framed the investment firm’s case for Hyperliquid around five qualities: product-market fit, open architecture, revenue-linked token value, regulatory tailwinds and grassroots adoption.

That analysis comes from a company with a direct commercial position in the market. On June 3, 2026, Grayscale launched the Grayscale Hyperliquid Staking ETF on Nasdaq under the ticker HYPG. The product provides investors with exposure to HYPE while seeking to capture rewards through participation in the network’s staking process.

HYPG launched with an annual sponsor fee of 0.29%, which Grayscale described as the lowest gross fee among U.S.-listed Hyperliquid exchange-traded products at the time. The fund’s SEC registration documents confirm the 0.29% fee and its objective of reflecting the value of the HYPE held by the trust, including eligible staking rewards, after expenses and liabilities.

Grayscale’s five-point thesis should therefore be read in the context of an active product issuer evaluating the asset underlying one of its own exchange-traded funds. That does not invalidate the data or Pandl’s analysis, but it makes the firm’s financial interest relevant when assessing its conclusions.

The five points are connected. Hyperliquid first built a trading product that people were willing to pay to use. It then opened parts of that infrastructure to outside developers, while directing part of protocol activity into a mechanism that buys and burns HYPE.

That combination is more informative than the fee number alone. It suggests Hyperliquid is attempting to become an underlying financial platform rather than remaining a single decentralized exchange for crypto perpetual futures.

The Fee Curve Is Hyperliquid’s Product-Market-Fit Evidence

Grayscale’s chart shows cumulative trading fees rising steadily from early 2025 through July 2026 rather than depending on one isolated burst of activity. Growth accelerated during the second half of 2025 and continued throughout the first half of 2026, eventually moving beyond $1.2 billion.

Fees provide a stronger test of demand than headline trading volume alone. Volume can be inflated by temporary incentives, automated strategies or unusually volatile markets. Fees show that traders were repeatedly willing to pay for execution.

Hyperliquid’s product combines a fully onchain order book with perpetual and spot trading. According to the official documentation, orders, cancellations, trades, funding calculations and liquidations are processed transparently through HyperCore, the network’s native trading layer.

The performance of that system allowed Hyperliquid to compete in a market historically controlled by centralized exchanges. Grayscale previously estimated that the platform processed approximately $2.9 trillion in perpetual futures volume and generated around $800 million in revenue during 2025.

The cumulative fee total should still be interpreted carefully. It represents gross fees paid through the platform, not corporate profit or money belonging directly to HYPE holders. Rebates, referral rewards, liquidity mechanisms and payments to outside market deployers affect how those fees are distributed.

The curve nevertheless indicates substantial recurring paid activity and provides clear evidence that Hyperliquid has found demand for its core trading product.

How Trading Activity Reaches the HYPE Token

Grayscale summarized the mechanism as a “buy-back-and-burn model where revenue loops straight back into token value accrual.”

The underlying mechanism is the Hyperliquid Assistance Fund. Under the protocol’s official fee rules, the fund automatically converts the fees allocated to it into HYPE as part of the network’s execution process. The acquired tokens are then burned, permanently removing them from circulating and total supply.

That creates a measurable connection between platform usage and HYPE:

1

Trading activity generates fees

2

Fees directed to Assistance Fund

3

Automatic HYPE token purchase

4

Tokens removed from supply (Burn)

The mechanism differs from a conventional dividend. HYPE holders do not receive cash distributions or acquire a legal claim on Hyperliquid’s revenue. Instead, trading activity creates recurring market demand for HYPE and reduces the number of tokens available.

The distinction prevents the $1.2 billion figure from being misread. It does not mean $1.2 billion has been returned directly to token holders or used entirely for burns. Hyperliquid’s fees are divided among community-controlled components, including the Assistance Fund, the Hyperliquid Liquidity Provider vault and third-party market deployers.

Spot and HIP-3 deployers may retain up to 50% of the fees generated by their markets. Maker rebates and other incentives also affect the final distribution.

HYPE’s value-accrual model therefore depends on more than cumulative historical fees. It requires trading activity to remain strong enough for future purchases and burns to continue. Falling volume, lower fee rates or a larger share of revenue going to outside builders would weaken the amount flowing through the Assistance Fund.

READ MORE:

Will HYPE Be the Smart Money Play in the Next Bull Run?

Will HYPE Be the Smart Money Play in the Next Bull Run?Open Architecture Expands the Fee Engine

Hyperliquid’s larger opportunity comes from allowing other teams to build on top of its trading and liquidity infrastructure.

Through HIP-3, qualifying developers can deploy their own perpetual futures markets while inheriting HyperCore’s order books, margin system and execution infrastructure.

A mainnet deployer must stake 500,000 HYPE and is responsible for defining and operating the market. That includes selecting the underlying price feed, setting leverage limits, maintaining oracle updates and settling the contract when necessary.

The stake is not merely an access fee. Deployers can be penalized for inputs that damage network performance or for operating markets with unreliable pricing. This allows listings to become more open without removing accountability from the teams creating them.

HIP-3 also changes Hyperliquid’s growth model. The core team no longer has to identify and operate every new market itself. Independent developers can introduce perpetual contracts tied to crypto assets, equities, commodities, indices and other instruments with suitable price feeds.

Hyperliquid benefits even when users access those markets through third-party applications. Its builder-code system lets trading terminals, wallets and mobile applications attach an approved fee to orders routed on behalf of their users.

That system allows independent teams to generate revenue from Hyperliquid’s liquidity without having to build a blockchain, matching engine and margin system from the ground up. It also gives the network a way to distribute its trading infrastructure through multiple interfaces rather than depending entirely on one application.

The HyperEVM extends the same strategy to smart-contract applications. Developers can deploy EVM-compatible protocols while connecting them to assets and liquidity available through the broader Hyperliquid network.

This produces the flywheel behind Grayscale’s open-architecture thesis:

More builders introduce additional markets and applications

Additional products bring new users and trading activity

Trading generates fees for builders and the protocol

Part of the protocol allocation purchases and burns HYPE

HYPE is also required for staking, market deployment and network activity

The architecture gives Hyperliquid room to grow beyond its original crypto perpetuals business. Whether the flywheel becomes durable will depend on the quality and sustained usage of the markets being launched, not simply their number.

Grassroots Growth Is Not the Same as Full Decentralization

Pandl’s fifth point concerns how Hyperliquid reached its current position.

Unlike many large crypto projects, Hyperliquid did not begin with a conventional venture-capital round. The Hyper Foundation describes the network as having no outside investors, no paid market makers and no fees directed to a company.

Grayscale also highlighted the distribution of roughly 30% of the HYPE supply to users at launch. That approach placed a substantial part of the network in the hands of people who had previously traded on the platform rather than selling it privately to early financial backers.

The lack of venture funding reduced Hyperliquid’s exposure to one common token-market risk: large early investor allocations becoming available for sale after lock-up periods expire. It also aligned the initial distribution more closely with actual platform usage.

“Grassroots” should not, however, be treated as a synonym for completely decentralized.

The SEC filings for Grayscale’s now-trading Hyperliquid Staking ETF identified approximately 24 validators as of April 30, 2026. The filings warned that the limited validator set could allow coordinated action over market parameters, bridges, withdrawals and incident responses.

They also noted that Hyperliquid Labs continued to exercise substantial influence over network development and that the network’s core protocol was not fully open source at the time of the filing.

Those factors do not erase the community-led launch, but they qualify the decentralization narrative. Hyperliquid combines broad token distribution and permissionless development with a comparatively concentrated validation and governance structure.

READ MORE:

Stablecoins Could Change How European Banks Fund Loans

Stablecoins Could Change How European Banks Fund LoansRegulation Is Both a Tailwind and a Competitive Threat

Grayscale’s regulatory argument became more concrete in May 2026, when the Commodity Futures Trading Commission approved a Bitcoin perpetual contract for listing by a registered U.S. derivatives exchange.

The agency also issued a policy statement establishing a case-by-case route for other perpetual contracts. In June, it sought public input on continuous trading and perpetual contracts tied to energy commodities.

These steps validate parts of the market structure Hyperliquid has been building: derivatives without fixed expiration dates, continuous trading and markets that remain available outside traditional exchange hours.

They do not constitute regulatory approval of Hyperliquid itself. The platform continues to restrict U.S. users, and registered American venues must comply with customer-protection, surveillance, reporting and risk-management requirements that do not apply in the same way to a protocol that is not registered as a U.S. derivatives venue.

Regulatory progress could also create stronger competitors. If established U.S. exchanges can list perpetual contracts and operate continuously, part of Hyperliquid’s product advantage may become available through regulated platforms with existing institutional relationships.

Hyperliquid’s regulatory engagement became more direct on July 14, 2026, when representatives connected to its ecosystem met with the SEC’s Crypto Task Force to discuss decentralized perpetual markets and the HIP-3 architecture. The meeting showed that the protocol’s market structure is now part of the regulatory conversation, but it did not constitute approval of Hyperliquid or create a lawful path for U.S. access.

The tailwind therefore supports the instrument more clearly than it supports one venue. Hyperliquid would benefit if regulators normalize perpetual futures and around-the-clock markets, but it would also face exchanges capable of offering similar products to institutions that require regulated access.

What Could Confirm Grayscale’s Hyperliquid Thesis

The next stage is proving that Hyperliquid’s architecture can generate durable activity beyond its core exchange.

Several developments would strengthen that case:

Fees continuing to rise without depending on one period of unusually high crypto volatility;

More trading activity coming from independently deployed HIP-3 markets;

Builder-code revenue expanding across multiple applications rather than remaining concentrated in a few interfaces;

Real-world asset and outcome markets retaining users after their initial launch periods;

A broader validator set and reduced dependence on coordinated intervention;

Regulatory progress that expands lawful access without forcing the network to abandon its onchain structure.

The weakest version of the thesis is that high trading fees automatically make HYPE more valuable. Fee generation alone cannot guarantee token performance, particularly if activity declines or the share reaching the burn mechanism falls.

The stronger version is that Hyperliquid has built a functioning exchange, a distribution system for independent applications and a token model that connects network usage with recurring purchases and supply reduction.

Grayscale’s five-point case ultimately depends on those elements continuing to develop together. The fee curve shows that the original trading product found demand. Open architecture must now demonstrate that Hyperliquid can support a durable ecosystem rather than a single successful venue.

Methodology: This analysis is based on Hyperliquid’s official protocol documentation, Grayscale Research, data attributed to Allium, and public filings and announcements from the U.S. Securities and Exchange Commission and the Commodity Futures Trading Commission. Figures and source documents were reviewed on July 18, 2026.

This article is provided for informational purposes only and does not constitute investment advice. Any financial interests or commercial relationships involving the publication or author should be disclosed separately where applicable.

The post Hyperliquid’s $1.2B Fee Engine Puts HYPE in Focus appeared first on Coindoo.