Key Highlights The Reserve Bank of India (RBI) has reportedly reiterated its preference for a crypto ban, according to internal documents cited by Reuters. The RBI wants banks and financial i

Key Highlights

- The Reserve Bank of India (RBI) has reportedly reiterated its preference for a crypto ban, according to internal documents cited by Reuters.

- The RBI wants banks and financial institutions barred from crypto exposure to avoid financial risks.

- Less than 25% of 645,000 crypto traders reported their transactions in FY23 tax returns.

- The RBI has maintained a cautious-to-hostile stance on cryptocurrencies since 2013.

India has nearly 39 million crypto investors holding approximately $2.1 billion in digital assets — and the institution responsible for the country’s monetary policy has spent 13 years trying to keep them out of the financial system. The latest Reuters report confirms that position has not softened. If anything, it has hardened.

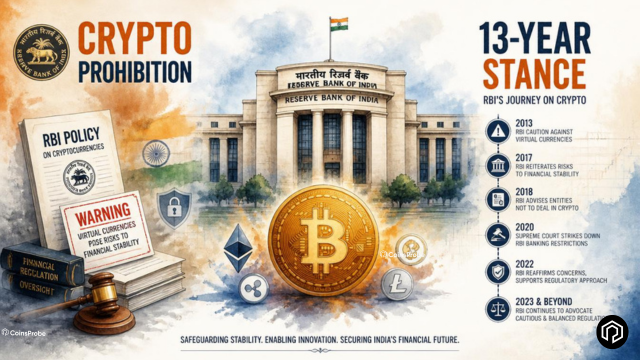

The RBI’s 13-Year Stance — A Verified Timeline

Understanding today’s news requires understanding that this is not a new development. According to insights from @simplykashif The RBI’s hostility toward cryptocurrency is one of the most consistent regulatory positions in global finance:

December 24, 2013 — RBI issued its first public advisory warning users, holders, and traders of virtual currencies including Bitcoin about potential financial, legal, and security risks. Bitcoin was trading below $1,000 at the time.

February 1, 2017 — RBI reiterated it had neither licensed nor authorised any entity to deal in virtual currencies — making clear that any crypto activity occurred entirely outside the regulated financial system.

December 5, 2017 — As Bitcoin’s price surged globally and Indian retail interest peaked, RBI repeated its warnings — consistent messaging across multiple years now.

April 6, 2018 — The most consequential early intervention: RBI issued a circular prohibiting all regulated entities — banks, NBFCs, and payment companies — from providing services to businesses or individuals dealing in virtual currencies. This was effectively a banking ban on crypto in India.

March 4, 2020 — The Supreme Court of India struck down the 2018 circular, ruling it disproportionate because the RBI had not demonstrated actual harm to any regulated entity. A landmark ruling — but one that did not change the RBI’s underlying position.

2021 onward — Despite the Supreme Court ruling, the RBI continued expressing serious reservations and advocating caution. Banks were clarified to be unable to deny services solely because customers dealt in crypto — but the RBI’s institutional preference remained clear.

2026 — Today’s Reuters report: RBI has again argued internally for a policy “leaning towards prohibition.”

Thirteen years. Multiple advisories, one outright banking ban, one Supreme Court reversal, and now a renewed push for prohibition. The RBI’s position has not been shaken by bull markets, institutional adoption globally, or regulatory clarity in other major economies.

What the Latest Internal Documents Show

According to internal government documents reviewed by Reuters, the July 2026 position involves two distinct institutional pushes:

The RBI’s position:

The central bank wants banks and financial institutions to be barred from holding, trading, or gaining any exposure to crypto assets and privately issued stablecoins. The specific concern framed is “contagion risk” — the possibility that crypto market volatility could transmit shocks into the regulated banking system if financial institutions have material exposure.

This is a more targeted version of the 2018 banking ban argument — the RBI is not necessarily calling for a blanket retail ban at this stage, but for a wall between the banking system and crypto specifically.

The tax department’s position:

India’s tax authorities have flagged what amounts to a compliance crisis. The scale of the problem in their own data:

- 645,000 individuals conducted crypto transactions in FY23

- Fewer than 25% reported those transactions in their tax returns

- Trading through offshore exchanges and private wallets makes transaction tracking “extremely difficult”

- Tax recovery from crypto gains remains structurally challenging under the current framework

India already has some of the world’s most aggressive crypto taxation — a 30% flat tax on crypto gains and a 1% TDS (Tax Deducted at Source) on transactions. Despite this, the compliance rate among crypto traders is under 25%. The tax department’s argument is that without structural enforcement mechanisms, the tax framework produces revenue on paper but not in practice.

Why the RBI Remains Cautious — The Four Concerns

The RBI’s position, across 13 years, has consistently rested on four core concerns:

Monetary sovereignty — Private stablecoins — particularly those denominated in foreign currencies — represent a direct challenge to the rupee’s role as India’s sole legal tender. From the RBI’s perspective, widespread adoption of a USD-denominated stablecoin by Indian users would effectively dollarise a portion of India’s domestic economy without any policy mechanism to control it.

Financial stability — The argument that crypto market volatility can transmit shocks to the regulated financial system — particularly if banks, NBFCs, or payment companies hold significant crypto exposure or serve crypto-heavy clients.

Tax compliance and AML — As the tax department data above illustrates — the current framework is producing substantial non-compliance. The combination of offshore exchange access, private wallets, and pseudonymous transactions creates an enforcement environment that traditional tax and AML tools are not well-suited for.

Valuation standards — The absence of uniform, regulated valuation standards for crypto assets makes them difficult to incorporate into regulated financial reporting, risk management frameworks, and prudential oversight.

The Current Legal Status — A Carefully Defined Grey Zone

Cryptocurrencies exist in an unusual legal position in India — one shaped by regulatory inaction as much as deliberate policy.

The Supreme Court’s 2020 ruling struck down the banking ban and established that crypto activity is not inherently illegal. But no subsequent legislation has either explicitly legalised or banned private cryptocurrencies. A 2021 draft bill that would have banned private cryptocurrencies and established a framework for a Central Bank Digital Currency was never introduced in Parliament.

The result: crypto exists in a grey zone where:

- Retail trading is not illegal but is heavily taxed

- Banks cannot deny services solely based on crypto activity

- Global exchanges like Binance and Coinbase can operate after registering with the Financial Intelligence Unit (FIU)

- No formal regulatory framework governing consumer protection, exchange operations, or institutional participation exists

The latest internal documents suggest that rather than moving toward a clear regulatory framework — as the EU has done with MiCA, the US is progressing toward with recent legislation, and Singapore has established with its MAS framework — India’s key agencies are leaning toward tighter curbs rather than structured regulation.

What This Means — Three Perspectives

For India’s 39 million crypto investors:

Continued regulatory uncertainty is the defining characteristic of crypto in India — and that uncertainty has a real cost. It limits institutional product development, suppresses mainstream exchange growth, and creates ongoing legal ambiguity for users who have no clear framework governing their rights or protections. A prohibition-leaning policy without formal legislation maintains this limbo indefinitely.

For the Indian crypto industry:

A formal prohibition would be devastating for the domestic exchange ecosystem and would likely accelerate capital and talent migration to more crypto-friendly jurisdictions. A regulatory framework — even a restrictive one — would at least provide a foundation for legal product development. The current grey zone with prohibition rhetoric is the worst of both worlds for legitimate industry participants.

For the Indian government:

The fiscal argument cuts both ways. Crypto’s 30% tax rate and 1% TDS are theoretically significant revenue sources — but the sub-25% compliance rate means the actual revenue collected is a fraction of what it could be. More effective regulation might produce more revenue than prohibition, which would simply push activity further underground or offshore. The government has not publicly resolved this tension.

Bottom Line

The RBI’s renewed push for a prohibition-leaning crypto policy in July 2026 is consistent with its 13-year institutional position — but it arrives in a significantly changed global context. Major economies including the EU, the UK, Singapore, Japan, and increasingly the United States have moved toward regulatory frameworks that acknowledge crypto’s existence and attempt to govern it. India remains the most prominent major economy still debating whether to prohibit it outright.

With 39 million investors and $2.1 billion in digital assets already present in the Indian market, prohibition-leaning policy creates a specific outcome: it does not eliminate crypto activity, it simply moves it offshore and underground — reducing tax compliance further while leaving investors with fewer protections than a regulated environment would provide.

The finance ministry and RBI have not issued public comments on the Reuters report. What happens next — formal legislation, continued grey zone, or actual prohibition — remains genuinely uncertain.

Disclaimer: The views and analysis presented in this article are for informational purposes only and reflect the author’s perspective, not financial advice. Technical patterns and indicators discussed are subject to market volatility and may or may not yield anticipated results. Investors are advised to exercise caution, conduct independent research, and make decisions aligned with their individual risk tolerance.

Read Also: Pi Network App Studio Adds Backend Support and AI Planning – What’s New