The global stablecoin market has long been a dollar-dominated space, and for good reason. The infrastructure, liquidity, and trust built around dollar-pegged coins took years to develop. Now

The global stablecoin market has long been a dollar-dominated space, and for good reason. The infrastructure, liquidity, and trust built around dollar-pegged coins took years to develop. Now Japan is stepping into the ring with something that could, at least in theory, start shifting some of that weight. SBI Group has officially moved to issue the JPYSC stablecoin, making it Japan’s first trust bank-backed yen stablecoin and the country’s clearest signal yet that it is serious about participating in the digital asset settlement economy at an institutional level.

What Exactly Is the JPYSC Stablecoin and Why Does It Matter?

Unlike most stablecoins that chase retail adoption through crypto exchanges and DeFi platforms, the JPYSC stablecoin is built with a different audience in mind entirely. SBI structured it through Shinsei Trust and Banking, which gave it the regulatory foundation needed to classify it under Japan’s Type III electronic payment instrument framework.

That classification is not just a bureaucratic detail. It means stronger investor protections, tighter compliance requirements, and a legal standing that most stablecoins operating globally do not have.

The JPYSC stablecoin targets large-volume settlement, treasury management, and tokenized asset infrastructure for financial institutions. Think of it less like Tether and more like JPMorgan’s JPM Coin, which operates quietly behind the scenes processing institutional payments rather than trading on public exchanges. That comparison matters because it sets realistic expectations about what JPYSC is actually trying to do.

Source DeFi Lama

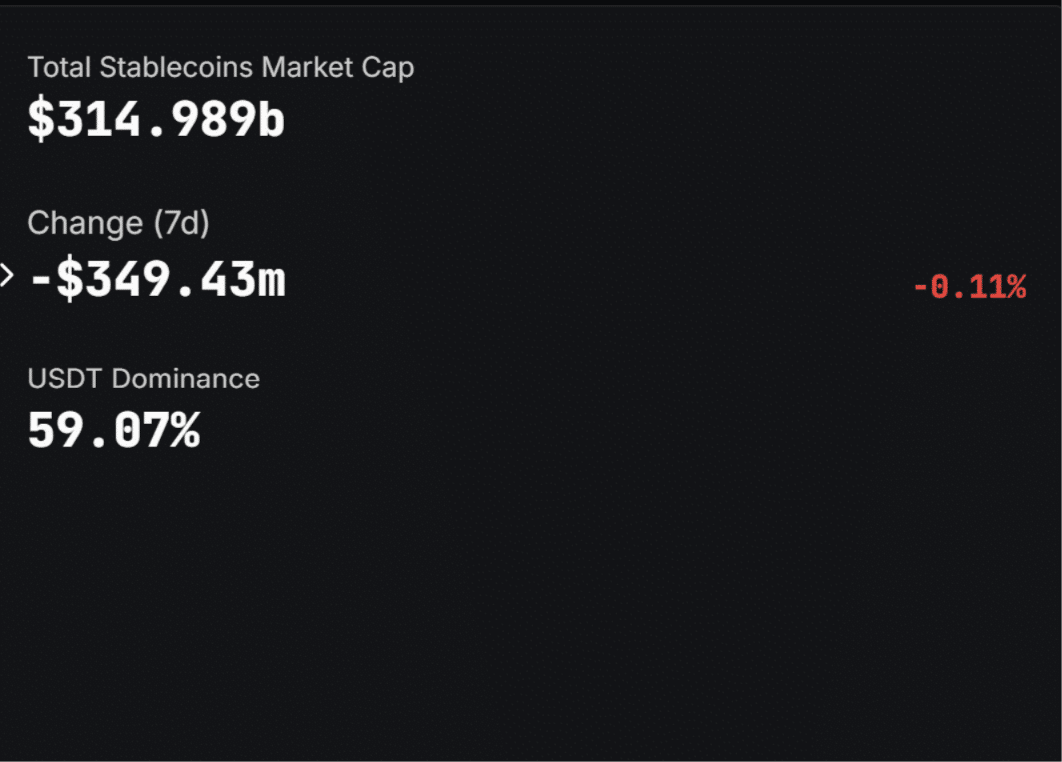

The Mountain It Has to Climb: USDT and USDC Control the Market

Here is where the numbers tell a sobering story. Tether currently holds over $186 billion in market capitalization, which accounts for roughly 59% of the entire $315 billion global stablecoin market. USD Coin adds another $74 billion on top of that. Together, dollar-denominated stablecoins control the overwhelming majority of cross-border digital payment flows, and yen-denominated liquidity on-chain barely registers in comparison.

The JPYSC stablecoin is not launching into a neutral environment. It is entering a market where dollar rails are deeply embedded into the workflows of financial institutions, crypto traders, and cross-border payment providers worldwide. Switching infrastructure is expensive, slow, and requires genuine incentive beyond regulatory compliance alone. That is the real challenge SBI faces, and no amount of institutional polish changes that fundamental reality.

Cross-Border Settlement: The One Use Case That Could Make JPYSC Relevant

Despite the uphill battle, there is a credible argument for why the JPYSC stablecoin could find meaningful traction in a specific corridor. Japan has significant trade and financial relationships across Southeast Asia, and yen-denominated settlement in those corridors generates real foreign exchange exposure for businesses operating on both sides.

Source Nikkei

If JPYSC can reduce that FX friction by allowing direct yen settlement on blockchain infrastructure without converting through dollars, that is a genuine cost-saving proposition.

That is not a guaranteed win. It requires liquidity depth, counterparty adoption on both ends, and seamless integration with existing banking systems. But it is the kind of use case that could justify why a regulated financial institution would choose JPYSC over USDC for a specific class of transaction, even if they keep using dollar stablecoins for everything else.

Early Signals and What to Watch Going Forward

The rollout of the JPYSC stablecoin has been intentionally controlled ahead of its anticipated Q2 2026 launch window, which means on-chain transaction volumes remain low at this stage. That is not necessarily a red flag. Institutional products typically go through quiet pilot phases before scaling, and early interest from financial institutions suggests the demand conversation is already happening behind closed doors.

The metrics that will matter most in the months ahead are transaction count, settlement volume, and whether cross-border flows start appearing in jurisdictions outside Japan. If JPYSC sees adoption purely within domestic Japanese banking infrastructure, it will remain a local product with limited global relevance. If international institutions begin routing yen-denominated settlements through it, that changes the conversation significantly.

Conclusion

The JPYSC stablecoin represents a well-structured, regulatory-first approach to digital asset settlement that reflects how seriously Japan is treating this space. SBI has done the groundwork, secured the legal framework, and targeted the right institutional audience.

Whether that translates into meaningful market share against USDT and USDC will depend entirely on adoption, and adoption requires institutions to see a tangible reason to move off the rails they already trust. That proof has not arrived yet, but the foundation is real, and the timing, given global interest in non-dollar settlement alternatives, is worth watching closely.

Frequently Asked Questions

What is the JPYSC stablecoin?

It is a yen-backed stablecoin issued by SBI Group through Shinsei Trust and Banking, designed for institutional payments and cross-border settlement on blockchain infrastructure.

Who is the JPYSC stablecoin designed for?

It targets financial institutions, not retail users, focusing on treasury operations, large-volume settlements, and tokenized asset transactions.

Can JPYSC compete with USDT?

Directly competing with USDT’s $186 billion market cap is unlikely in the near term, but JPYSC could carve out a niche in yen-denominated institutional settlement corridors, particularly across Asia.

When is JPYSC expected to launch fully?

The anticipated timeline points to Q2 2026, though early rollout has been controlled and volumes remain low at this stage.

Glossary of Key Terms

Stablecoin: A digital asset designed to maintain a stable value by being pegged to a real-world currency or asset, such as the US dollar or Japanese yen.

Market Capitalization: The total market value of a cryptocurrency, calculated by multiplying the current price by the total circulating supply.

Cross-Border Settlement: The process of completing financial transactions between parties in different countries, often involving currency conversion and clearing.

Type III Electronic Payment Instrument: A Japanese regulatory classification for digital payment instruments that includes specific compliance, transparency, and investor protection requirements.

Tokenized Assets: Real-world financial assets, such as bonds or securities, that are represented as digital tokens on a blockchain network.

Read More:Is Japan’s JPYSC Stablecoin the Biggest Threat to USDT in 2026?">Is Japan’s JPYSC Stablecoin the Biggest Threat to USDT in 2026?