The ban, tucked into the 21st Century ROAD to Housing Act, is the first of its kind passed by Congress. It bars the Federal Reserve from issuing or creating a CBDC, or any substantially simil

The ban, tucked into the 21st Century ROAD to Housing Act, is the first of its kind passed by Congress. It bars the Federal Reserve from issuing or creating a CBDC, or any substantially similar digital asset, through December 31, 2030, and requires explicit congressional authorization for any digital dollar effort after that date.

Key Takeaways

- The Senate passed H.R. 6644 in an 85-5 vote on June 22, and the House cleared the amended version 396-13

- The CBDC prohibition, contained in Section 1101 of the enrolled bill, runs through December 31, 2030

- The law exempts any dollar-denominated currency that is open, permissionless, and private, leaving stablecoin issuers untouched

- The bill sat on Trump’s desk for the maximum 10 days, excluding Sundays, before becoming law without action

A Crypto Ban Delivered Through a Housing Package

The prohibition traveled inside legislation that has nothing to do with digital assets. The act is primarily a bipartisan package meant to boost housing supply and stop large investors from buying up single-family homes, and the anti-CBDC language was inserted to secure House Republican support for passage, as CoinDesk reported when the Senate cleared the measure.

The statutory text states that the Fed “may not issue or create a central bank digital currency or any digital asset that is substantially similar,” whether directly or through an intermediary bank. Even after the ban lapses at the end of 2030, the central bank would need explicit congressional authorization to pursue a digital dollar.

The carve-out matters as much as the prohibition. By exempting open, permissionless, and private dollar assets, the law shields issuers such as Circle and Tether, which already operate under the GENIUS Act framework adopted in 2025. Read together, the two laws define Washington’s digital-dollar posture: regulated private stablecoins are the sanctioned channel, and the Fed is legally sidelined until 2031 at the earliest.

How the Law Passed Without a Signature

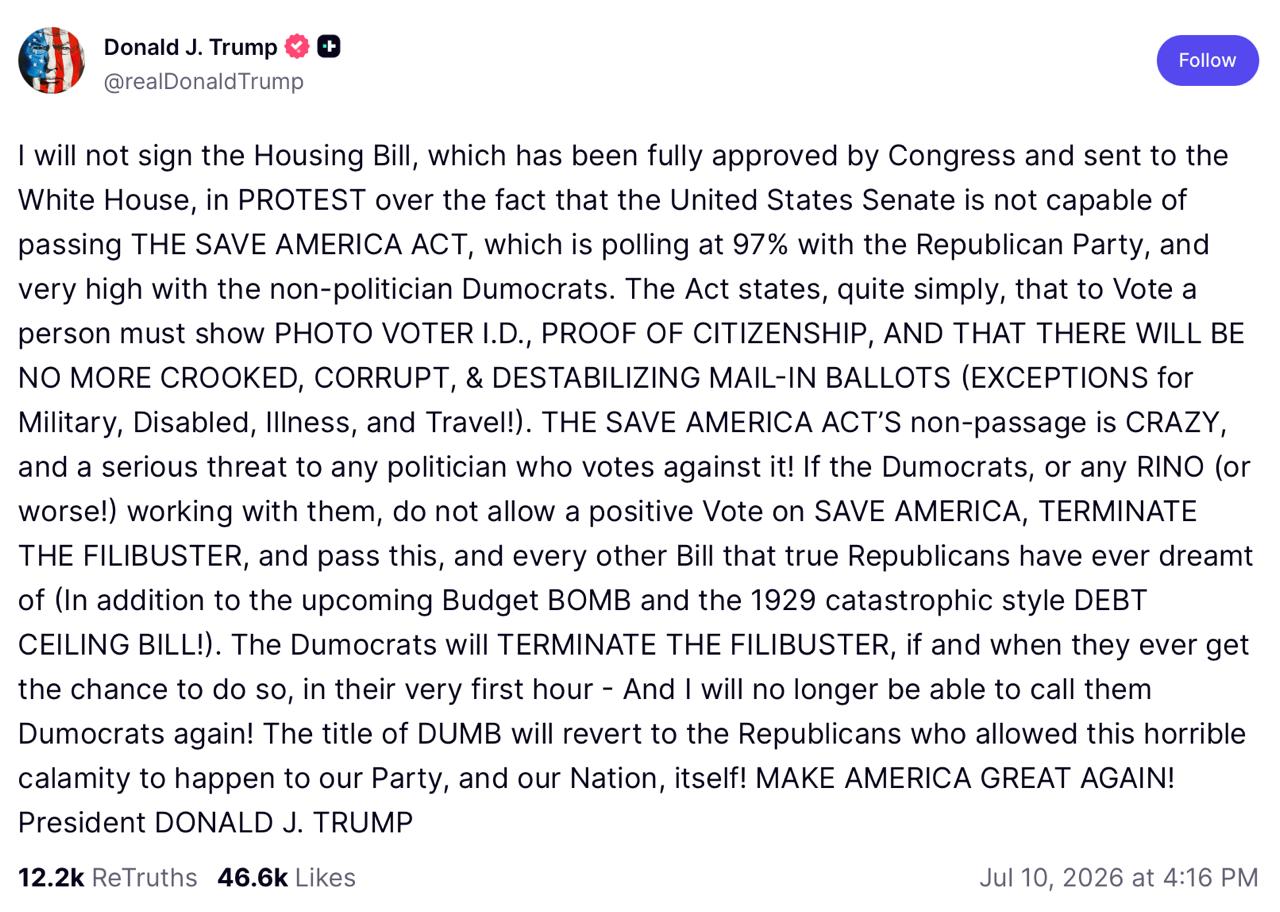

Trump announced his refusal in a Truth Social post on July 10, writing that he would not sign the bill “in PROTEST over the fact that the United States Senate is not capable of passing THE SAVE AMERICA ACT,” his preferred voter-ID legislation. The post did not mention the CBDC provision at all.

Refusing to sign is not the same as vetoing. Under Article I, Section 7 of the Constitution, a bill presented to the president becomes law automatically after 10 days, excluding Sundays, unless it is vetoed. The bill reached Trump’s desk on June 29, and the clock ran out at midnight into Saturday, July 11. A veto was never realistic in practice: the House and Senate margins were far above the two-thirds threshold needed for an override.

The result is an unusual legal artifact. Trump’s own January 2025 executive order already barred any effort to establish, issue, or circulate a CBDC across US jurisdiction, yet the statutory version now on the books entered force over his objection to the vehicle carrying it. The distinction is not cosmetic. An executive order can be reversed by the next administration with a signature; the new prohibition survives any change in the White House through the end of 2030.

What the Ban Does Not Change

The practical near-term impact on Fed policy is limited, because neither the Federal Reserve nor Congress had been pushing to develop a CBDC. The Fed had stated it would only issue one if Congress authorized it, meaning the law codifies an existing standstill rather than halting an active program.

The prohibition is also temporary, a point that has already divided its supporters. Some House conservatives argued the freeze should be permanent, with Rep. Anna Paulina Luna saying “CBDCs are bad for everyone,” according to Yahoo Finance. A future Congress could let the sunset arrive quietly in 2030 or extend it, and that decision could fall to a very different political majority.

The sharper takeaway for the digital-asset industry may be procedural. Trump’s willingness to withhold a signature from broadly bipartisan legislation over an unrelated demand introduces a variable for the crypto bills still moving through Congress, including the CLARITY Act, which is expected to reach the Senate floor in July. Passage through both chambers no longer guarantees a smooth final step.

READ MORE:

GRAM at $1.6: Why the Hype Faded and Reality Took Over

GRAM at $1.6: Why the Hype Faded and Reality Took OverThe US Now Moves Against the Global Current

The statutory freeze puts the United States on the opposite trajectory from other major economies. The European Central Bank is preparing a digital euro, with a pilot expected next year and a full launch targeted for 2029, while China signed up 26 financial institutions to its e-CNY cross-border platform this month. Three countries have launched a CBDC and dozens more are piloting or developing one, according to the Atlantic Council.

Until the end of 2030, dollar-denominated digital payments innovation in the US belongs by law to the private sector. Whether that structure persists past the sunset depends on the Congress seated at that point, not the one that wrote the ban.

The information provided in this article is for informational purposes only and does not constitute financial, investment, or legal advice.

The post US CBDC Ban Becomes Law Without Trump’s Signature appeared first on Coindoo.