The latest data published by Dune Analytics reveal an important fact: stablecoins are entering a new phase of their development. Indeed, USDT and USDC are no longer seeking to dominate the sa

The latest data published by Dune Analytics reveal an important fact: stablecoins are entering a new phase of their development. Indeed, USDT and USDC are no longer seeking to dominate the same markets. The former establishes itself as the reference for payments. The latter, on the other hand, consolidates its place at the heart of DeFi. Analysts therefore agree on one point: this evolution could permanently transform the crypto ecosystem. More details in the following paragraphs!

In Brief

- Stablecoins no longer engage in a direct war: their uses are specializing.

- USDT concentrates the bulk of crypto payments, with nearly 95 billion dollars in commercial transactions observed.

- USDC maintains its lead in DeFi, exchanges, and dApps.

- The Tron, Ethereum, and Base networks play a decisive role in this distribution.

- This evolution could redefine global stablecoin adoption and accelerate their integration into financial infrastructures.

USDT Establishes Itself as the King of Stablecoin Payments

The data compiled by Dune Analytics indicate that USDT issued by Tether reigns supreme in the commercial transactions segment. Just in the first half of 2026, it represents about 95 billion dollars in stablecoin payments (compared to only 14 billion dollars for USDC). This amounts to a ratio close to 7 to 1.

That’s not all! The Tether stablecoin also captures nearly 92% of the 48 billion dollars in inter-company payments (B2B) volume alone during the same period.

Crypto analysts agree on this: if USDT currently outperforms its competitors in the stablecoin payment market, it is mainly thanks to the success of the Tron crypto network. About 93% of Tether’s total circulating supply is indeed held in private wallets rather than on exchanges or within complex protocols.

Breakdown: USDT stablecoins primarily serve as an accessible store of value, cross-border fund transfer instrument, and direct payment method for international trade. This illustrates concrete adoption. More importantly, this performance shows that Tether is now establishing itself as the monetary infrastructure of emerging markets.

Good to know: in June, USDT briefly surpassed Ethereum in terms of market capitalization.

Your 1st cryptos with SwissborgThis link uses an affiliate program.USDC Becomes the Preferred Stablecoin of DeFi

According to the Dune analysis report, Circle’s USDC rises to the rank of reference asset for:

- liquidity providers;

- lending platforms;

- algorithmic traders.

Specifically, the data report a massive concentration of USDC stablecoins on the Ethereum networks as well as its main growth layer 2, Base. In June 2026, for example, the USDC transfer volume on the Base crypto network reached a historic peak of 2.6 trillion dollars. This is the highest figure of all token-blockchain pairs tracked by Dune.

Even more interesting! During the same period, this digital asset processed 1.6 trillion dollars in transactions on Ethereum.

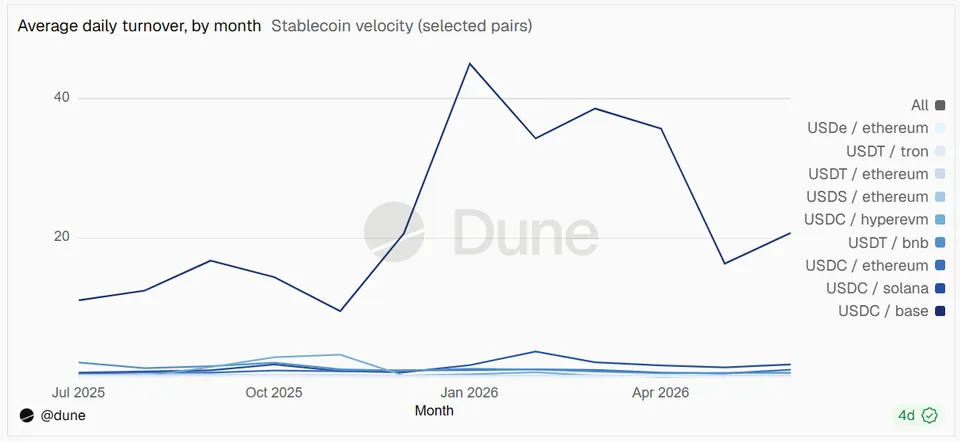

But Dune’s analysis reveals another key indicator: financial velocity. On Base, USDC indeed records a daily velocity equivalent to about 20 times its circulating supply. This means that a single digital dollar unit from Circle is reused on average twenty times per day across various smart contracts, yield loops, and DEX.

Unlike USDT, USDC stablecoins circulate mainly within an ecosystem where capital is constantly reallocated between different protocols. Simply put, they primarily feed on on-chain liquidity.

Chart showing the velocity of stablecoins (Source: Dune)

Chart showing the velocity of stablecoins (Source: Dune)A Historic Concentration That Redefines the Crypto Market Structure

The Dune analysis result confirms an important point: the stablecoin market is entering a maturity phase. The days when USDT and USDC fought a sterile duel are now over. Today, the two main stablecoin issuers no longer compete for the same market shares. They extend their respective monopolies over distinct territories. Thus, each asset gradually develops a specialization.

Note that together, Tether and Circle now control nearly 83% of a global sector market capitalization amounting to 315 billion dollars. This calculation is based on tracking more than 200 stable assets across multiple blockchain networks.

To summarize this reversal, Dune CEO Fredrik Haga declared at the ETHCC 2026 held in Cannes:

The train is now moving.

For investors, the evolution of the stablecoin market shows that several players coexist today by responding to distinct needs:

- On one side, USDT establishes itself as the preferred asset for international payments, fund transfers, and daily settlements.

- On the other, USDC becomes an essential component of DeFi protocols, trading platforms, and new financial services built on the blockchain.

The key indicators now include transaction volumes, token circulation speed, liquidity depth, as well as diversity of use cases. In other words, stablecoin adoption no longer depends solely on their size. It also (and especially!) depends on their capacity to respond effectively to specific needs within the crypto ecosystem.

This Segmentation of the Stablecoin Market Complicates the Task for US Regulators

Signed in June 2025, the GENIUS Act creates the first federal framework for payment stablecoins. Thanks to this law, banks have the possibility to issue digital assets pegged to the dollar. The CLARITY Act, meanwhile, defines the intervention areas of the SEC and the CFTC. It was adopted by the Senate banking committee in May by a vote of 15 to 9. Since then, it has faced persistent resistance.

Three unresolved disagreements indeed prevented the vote before July 4:

- ethical obligations;

- protection of DeFi developers;

- stablecoin yield rules.

The Senate resumes activity on July 13, with about three useful weeks before the August recess. Without a clear framework distinguishing a payment stablecoin from a stablecoin massively used in DeFi, regulatory uncertainty could weigh on the entire sector.

What Future for Stablecoins Facing Growing Institutional Demand?

According to the Dune analysis report, the evolution of the stablecoin market towards segmentation by use is probably just a stage. It could even intensify further in the coming years, propelled by:

- the rise of digital payments;

- asset tokenization;

- the arrival of new institutional players.

These are all factors that should reinforce differentiated uses of the main stablecoins.

That’s not all! The boundary between payment and DeFi could also be redrawn if new issuers target specific niches like inter-company payments or institutional liquidity.

For Tether, the challenge will be to consolidate its lead in payments while supporting the expansion of digital economies. For Circle, the priority will probably remain the integration of USDC into decentralized finance infrastructures and regulated financial services.

In any case, the split in the stablecoin market demonstrates the maturity of the crypto ecosystem. It remains to be seen whether the emergence of CBDCs will disrupt this perfectly orchestrated private equilibrium. Knowing that the latter are not unanimous either.