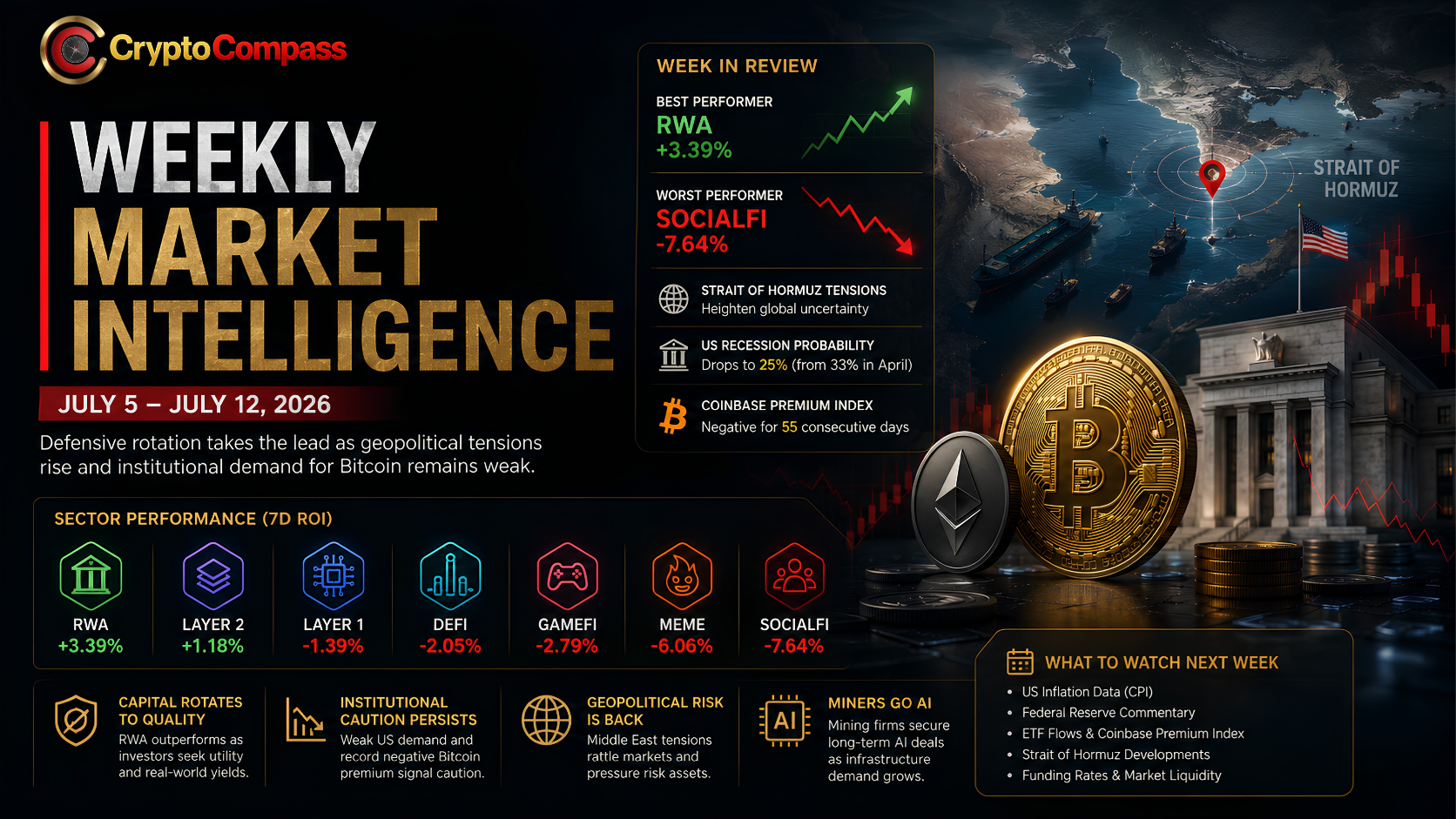

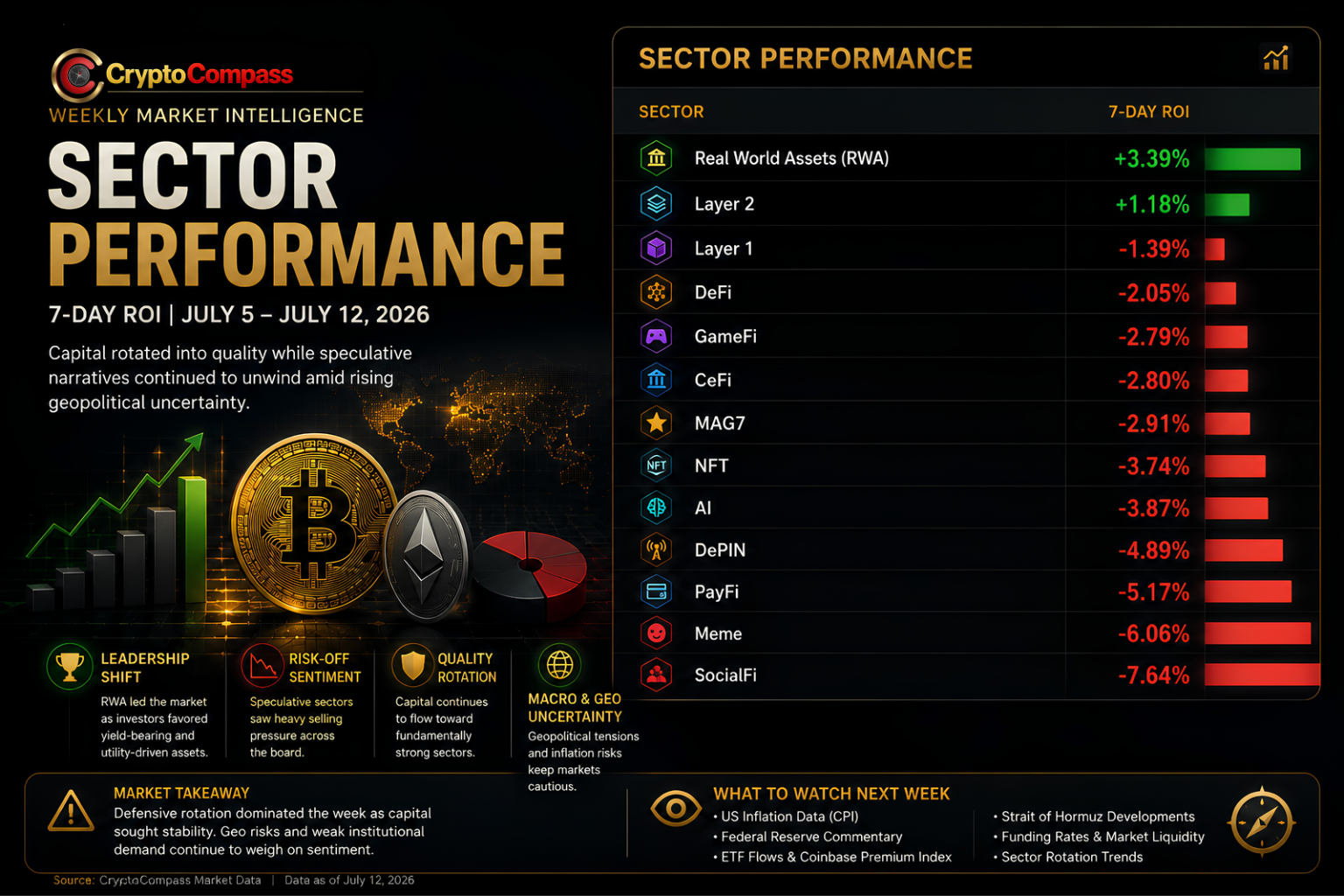

RWA led all crypto sectors with a weekly gain of 3.39%, extending its reputation as one of the strongest narratives throughout 2026.

A

AnonymousCryptoCompass newsroom

July 12, 2026

7 min read

ANALYSIS

CryptoCompass editorial visual for markets coverage.

The crypto market closed the second week of July with a clear divergence between defensive capital allocation and speculative positioning. While Real World Assets (RWA) emerged as the week's strongest-performing sector, capital continued flowing out of higher-beta narratives such as Meme, SocialFi and DePIN. At the same time, geopolitical tensions in the Middle East, weakening institutional demand for Bitcoin and shifting macroeconomic expectations combined to create one of the most cautious market environments since the second quarter.

Rather than witnessing a broad market correction, investors rotated toward sectors perceived to offer stronger fundamentals, sustainable cash flow and long-term utility. This defensive rotation increasingly resembles patterns typically observed during late-cycle market consolidation, where liquidity concentrates in higher-quality assets before expanding back into riskier segments.

Executive Summary

RWA led all crypto sectors with a weekly gain of 3.39%, extending its reputation as one of the strongest narratives throughout 2026. Layer 2 was the only other major sector finishing the week in positive territory, while nearly every speculative sector ended lower. Meme tokens declined 6.06%, DePIN lost 4.89%, AI retreated 3.87%, and SocialFi became the week's weakest performer with a 7.64% decline.

Meanwhile, geopolitical uncertainty intensified after renewed tensions surrounding the Strait of Hormuz, increasing global risk premiums across financial markets. Although economists have become more optimistic about avoiding a U.S. recession, expectations for persistent inflation continue supporting a "higher-for-longer" interest rate environment, limiting appetite for speculative assets.

Bitcoin itself remained trapped in a difficult position. The Coinbase Premium Index stayed negative for 55 consecutive days, marking the longest negative streak on record and suggesting continued institutional caution among U.S. investors.

Market Regime: Defensive Rotation Continues

The dominant market theme throughout the week was not panic selling, but selective capital rotation.

Investors increasingly favored sectors capable of generating real economic value rather than relying purely on narrative-driven momentum. Real World Assets continued attracting capital as tokenized Treasury products, private credit and institutional yield strategies gained further acceptance. Unlike previous bull cycles dominated by speculative narratives, 2026 increasingly resembles an environment where revenue-generating protocols outperform attention-driven assets.

Layer 2 networks also demonstrated relative resilience despite broader market weakness. Lower transaction costs, expanding developer ecosystems and continued Ethereum scaling adoption allowed the sector to outperform most of the market.

Conversely, speculative themes suffered broad liquidation. SocialFi remains under pressure as user growth stagnates across multiple platforms. Meme coins experienced another week of declining liquidity as retail participation cooled considerably compared with earlier quarters. DePIN also corrected despite maintaining one of crypto's strongest long-term infrastructure narratives, illustrating that even fundamentally attractive sectors are not immune during periods of tightening liquidity.

Although DeFi recorded a modest weekly decline, its longer-term trend remains impressive. Relative to Bitcoin, DeFi has outperformed by more than 57% year-to-date, highlighting that the sector continues attracting structural capital despite short-term corrections. RWA and SocialFi also remain positive against Bitcoin on a year-to-date basis, suggesting leadership is increasingly concentrated rather than broadly distributed.

Bitcoin: Institutional Demand Remains Weak

One of the week's most closely watched indicators continued flashing caution.

The Coinbase Bitcoin Premium Index remained negative for 55 consecutive trading days, the longest continuous stretch since the metric began tracking institutional buying behavior. Historically, extended negative readings indicate reduced demand from U.S.-based institutional investors, particularly ETFs, hedge funds and asset managers executing through Coinbase.

Although Bitcoin volatility has declined substantially compared with previous market cycles, lower volatility alone has not been sufficient to attract aggressive institutional accumulation. According to Real Vision analyst Jamie Coutts, Bitcoin may be entering the final stages of a prolonged bear-market structure where downside momentum continues weakening but trend confirmation has yet to emerge.

From a technical perspective, reduced volatility often precedes major directional moves. However, without improving spot demand or stronger ETF inflows, Bitcoin may remain range-bound until macroeconomic conditions become more supportive.

Macro Environment: Geopolitics Returned To Center Stage

Global macro developments once again played an outsized role in shaping crypto sentiment.

Escalating tensions between the United States and Iran raised concerns over potential disruptions to the Strait of Hormuz, one of the world's most strategically important energy shipping routes. Although maritime authorities reported that limited commercial traffic continued through southern channels, shipping activity declined sharply as operators reassessed operational risks.

Any sustained disruption to global energy supply chains would likely increase inflationary pressure worldwide, complicating monetary policy decisions for major central banks. For crypto markets, higher geopolitical uncertainty generally translates into tighter liquidity conditions and lower investor risk tolerance.

On the economic front, a Wall Street Journal survey suggested the probability of a U.S. recession has fallen to 25%, improving from 33% in April. Nevertheless, economists simultaneously revised inflation expectations higher, forecasting annual CPI around 3.4%, reinforcing expectations that the Federal Reserve may maintain elevated interest rates for longer than markets previously anticipated.

This combination of slowing recession fears but persistent inflation creates a difficult environment for speculative assets. While economic resilience supports corporate earnings and employment, prolonged higher interest rates continue reducing liquidity available for high-risk investments, including digital assets.

Institutional Trends

Institutional positioning remained mixed throughout the week.

One of the most discussed on-chain developments involved early Bitcoin advocate Peter Saddington. Blockchain data revealed that thirteen wallets accumulated approximately 250.3 million WEN tokens shortly after launch before transferring the holdings into a wallet associated with Saddington. The position now represents roughly 25% of WEN's total supply, highlighting both concentrated ownership and limited market liquidity.

Meanwhile, the Bitcoin mining industry continued accelerating its transition toward artificial intelligence infrastructure.

Although the TEM AI Infrastructure Growth Index declined roughly 16% over the past month, major mining companies including TeraWulf, Riot Platforms and Cipher Digital increasingly emphasized AI compute services as future revenue sources. TeraWulf's newly announced 20-year infrastructure agreement with Anthropic represents one of the strongest signals yet that mining operators increasingly view AI data centers as a long-term diversification strategy beyond Bitcoin mining alone.

Chinese manufacturers are expected to reach production capacity approaching 100,000 humanoid robots annually by the end of 2026, potentially exceeding the pace previously projected for several Western competitors. The rapid expansion has sparked renewed investor interest across semiconductor, battery and industrial automation supply chains, with companies including Hyundai Mobis and LG Energy attracting increased attention.

While not directly impacting cryptocurrency markets today, the convergence between AI infrastructure, robotics and decentralized computing may become an increasingly important investment theme over the coming years, particularly for sectors such as DePIN and decentralized GPU networks.

What To Watch Next Week

Investors should closely monitor several developments that could determine crypto market direction over the coming week:

U.S. CPI inflation data and its implications for Federal Reserve policy.

Any escalation or de-escalation surrounding the Strait of Hormuz.

Bitcoin ETF inflows and institutional spot demand.

The Coinbase Premium Index for signs of renewed institutional accumulation.

Treasury yields and the U.S. Dollar Index, both of which remain critical drivers of global liquidity.

Continued capital rotation between defensive sectors such as RWA and higher-beta narratives including AI, Meme and SocialFi.

Outlook

This week's market reinforced one of the defining themes of 2026: capital is becoming increasingly selective. Rather than chasing speculative narratives indiscriminately, investors are concentrating exposure in sectors with measurable utility, sustainable revenue models and stronger institutional adoption. Real World Assets continue benefiting from this structural shift, while DeFi maintains impressive year-to-date relative strength despite recent consolidation.

Bitcoin remains the market's primary uncertainty. Declining volatility suggests selling pressure may be fading, yet prolonged weakness in institutional demand indicates conviction has not fully returned. Combined with geopolitical uncertainty and a "higher-for-longer" monetary policy backdrop, the market is likely to remain driven by sector rotation rather than broad-based bullish momentum.

For now, the evidence suggests crypto has entered a phase where quality matters more than hype. Investors who focus on capital flows, macro conditions and institutional positioning may be better equipped to navigate the next major move than those relying solely on short-term price action.

Disclaimer: This report is for informational purposes only and does not constitute investment advice. CryptoCompass reviews the most important developments across the digital asset market over the past week, analyzing sector performance, macroeconomic developments, institutional positioning and on-chain activity to identify the trends driving crypto markets.

Ironwood formal verification aims to eliminate counterfeiting risks and restore confidence in Zcash. Stronger security upgrades and privacy features could support long-term ZEC adoption. ZEC

What to Know SXT has rebounded from its recent lows and broken above the Bollinger Band midpoint, signaling renewed buying momentum. RSI has climbed to 62, indicating bullish strength, though

You can also read this news on BH NEWS: Uniswap’s Strategic Alliance Sets New Trading Milestones Uniswap’s recent integration with Robinhood Chain has sparked significant growth in daily trad