Markets7 min read

Weekly Market Recap | July 5 – July 12, 2026

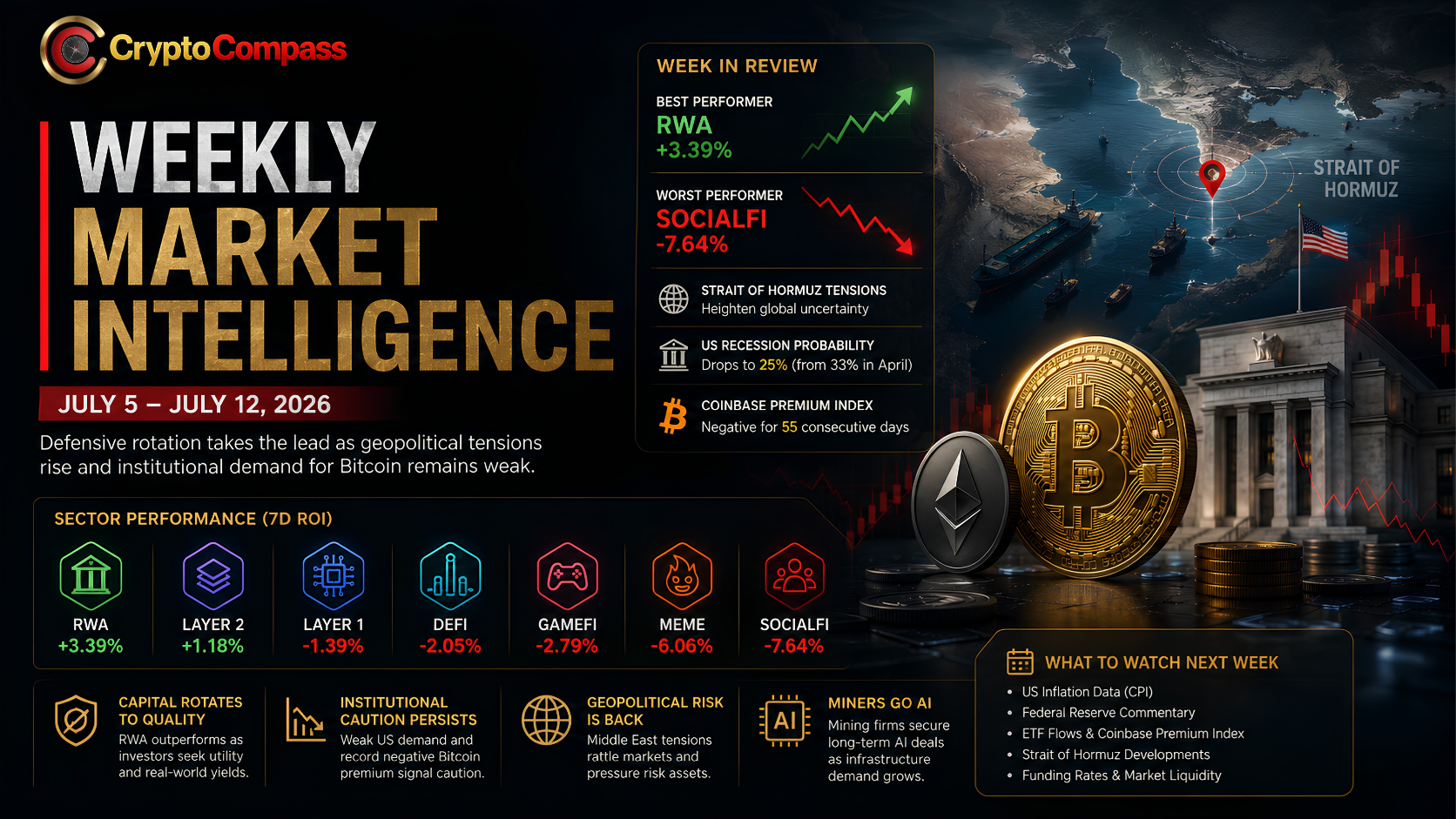

RWA led all crypto sectors with a weekly gain of 3.39%, extending its reputation as one of the strongest narratives throughout 2026.

The headline was easy to miss in a noisy week, but the move was anything but small: Empery Digital offloaded 1,400 BTC since May 7 for roughly $87.1 million. That cash is steering the firm in

The headline was easy to miss in a noisy week, but the move was anything but small: Empery Digital offloaded 1,400 BTC since May 7 for roughly $87.1 million. That cash is steering the firm into AI infrastructure, not out of crypto.

Part of the proceeds went straight to trimming liabilities. Another chunk is earmarked for a big bite of a Midwest data-center property that will host AI workloads. The company still holds a meaningful BTC stack and a thick cash cushion after the rotation.

This is the strategy shift a lot of treasury teams are quietly stress testing: turning volatile crypto assets into steady, power-and-rack revenue streams.

Empery Digital’s sale and redeployment is one snapshot of a wider turn. Bitcoin-heavy treasuries are bumping into a familiar problem: mark-to-market swings look great on the way up and brutal on the way down, while AI infrastructure needs dollars today and power contracts locked for years. Sell some BTC, secure compute, and try to build recurring cash flow. That’s the playbook.

Bitcoin is a high-octane treasury asset; AI infrastructure is a cash-flow asset. Rotations between the two are balance-sheet risk management in motion.

Here’s what Empery actually did, what it signals to markets, and how to think about similar moves from other firms sitting on BTC.

Across two months, Empery sold 1,400 BTC at an average price around 62,200 dollars per coin, raising roughly 87.1 million dollars according to Decrypt. On July 7, a 10 million dollar debt repayment posted, per The Block. And on June 30 the firm disclosed a 65 million dollar commitment for a 25 percent stake in a Midwest AI data-center property via Empery Digital investor relations (press release, June 30, 2026).

By July 10, Empery reported it still held 1,514 BTC and approximately 73.9 million dollars in cash, again via Decrypt. In other words, this wasn’t an exit from Bitcoin. It was a portfolio rebalance to raise dollars for infrastructure and de-risk the balance sheet.

AI data centers convert capex into contracted revenue. Think multi-year colocation and compute hosting agreements, power pass-throughs, and service tiers. For a treasury desk tired of marking BTC to market every quarter and explaining swings to investors, that kind of predictability can be a relief.

There’s also a race for power and GPUs. Leasing a slice of a facility or taking an equity stake in one is a way to secure both. If your corporate strategy touches AI workflows at all, or you believe compute resale has pricing power, getting into the stack early can be worth giving up some upside from BTC.

Finally, creditors and rating models often treat recurring infrastructure cash flows more favorably than a volatile crypto position. Swapping a portion of BTC into tangible assets and contracted revenue can improve leverage and coverage metrics. That may lower financing costs elsewhere.

Empery sold BTC. Another common route is borrowing against BTC or raising equity. Each path carries different costs and headaches. Here’s a quick way to stack them up without the spreadsheets.

Funding path Cash upfront Cost over time Balance sheet impact Key risks When it fits Sell BTC Immediate, full proceeds No interest; potential tax bill Reduces BTC asset; increases cash Lost BTC upside; execution timing Need dollars now; want simpler accounting Borrow vs BTC Quick if collateralized Interest plus fees BTC pledged; leverage increases Liquidation risk; margin calls Confident in BTC price; want to keep exposure Issue equity Depends on market appetite Equity dilution; no interest More shares; potential cash runway Valuation pressure; investor relations Strong equity market window

AI buildouts demand cash at milestones: land or lease, interconnects, generators, transformers, racks, cooling, networking, GPUs, staffing. If you think BTC could chop or draw down, the last thing you want is a margin call mid-construction. Selling avoids collateral risk and simplifies vendor payments.

Empery still holds 1,514 BTC and nearly 74 million dollars in cash based on July 10 reporting via Decrypt. That’s a sizeable treasury position by any standard. The sales appear paced over weeks, not a single dump, which tends to blunt market impact.

Expect more of this mixed playbook. Some firms will borrow against BTC to avoid selling. Others will sell a slice to ensure clean, unencumbered dollars for power deposits and gear. The common thread is using BTC strength to secure assets with steadier cash yields.

Data centers line up contracts that can span three to ten years, adjusted for power. That transforms lumpy capex into semi-predictable revenue. If utilization runs hot, incremental returns can look good relative to sitting in cash or taking on more BTC volatility.

The Midwest angle matters. Power pricing, grid interconnections, and land costs can still pencil out in parts of the region. Locating near fiber routes and utility substations can shave time-to-revenue. For a treasury team, that shortens the period between cash out and cash back in.

AI demand might cool, and hardware pricing can bite, but a well-sited facility with smart contracts can hedge some of that. The risk isn’t gone, just reshaped from price risk on BTC to utilization and power risk in data centers.

Large corporate sales matter less if executed gradually. Order book depth, OTC channels, and derivatives hedges can absorb supply when it’s handled professionally. The more important market signal is that BTC is evolving into a working capital source, not just a passive bet.

If facility stakes begin to throw off steady cash, expect investors to ask whether that cash could outperform a hold-only BTC strategy. That question alone nudges more CFOs to model rotations when BTC rallies and to re-accumulate on drawdowns. It introduces a new rhythm to treasury flows.

If more crypto-native treasuries rotate into compute, watch power markets and GPU supply chains. The next chokepoints won’t be on exchanges. They’ll be transformers, switchgear, and interconnect queues.

Rotating from BTC to AI infra doesn’t kill risk, it trades price volatility for construction, power, and utilization risk. Model all three before moving.

If you want ongoing coverage of treasury shifts like this, we track them closely at Crypto Daily, pairing on-chain footprints with corporate filings and deal flow.

No. The company sold 1,400 BTC to raise dollars but still held 1,514 BTC as of July 10 along with roughly 73.9 million dollars in cash, per Decrypt. That reads as a rebalance, not an exit.

Selling eliminates collateral and liquidation risk during a capex-heavy build. Borrowing can preserve upside but adds interest expense and the risk of margin calls if BTC dips. For a project with tight construction timelines, clean dollars are often easier.

A 65 million dollar committed investment for a 25 percent stake in a Midwest AI data-center property, disclosed June 30 in a company press release (Empery Digital investor relations). The firm also repaid 10 million dollars of debt on July 7, according to The Block.

Large sales can pressure price if they hit the market all at once. Empery’s selling occurred over weeks, which typically reduces market impact. Market structure, OTC flows, and hedging matter more than the headline number.

It’s likely some will. BTC gives treasuries an option to raise cash quickly when windows open. AI infrastructure offers contracted revenue. The mix of the two will depend on project quality, power access, and where the BTC price cycle sits.

Yes, if cash flows ramp and the balance sheet allows. Some firms treat BTC as a tactical treasury asset, scaling exposure up or down around capex cycles and market conditions.

Project milestones, signed tenants, power arrangements, and any updates to Empery’s BTC and cash balances. Those will show whether the pivot is translating into durable returns.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.