What Is Mutuum Finance (MUTM) Crypto lending often still runs through banks or centralized platforms. That setup adds fees, delays, and counterparty risk. It wants to remove that middle layer

What Is Mutuum Finance (MUTM)

Crypto lending often still runs through banks or centralized platforms. That setup adds fees, delays, and counterparty risk. It wants to remove that middle layer.

The protocol is a decentralized, non-custodial lending platform. According to the official website, it lets users lend, borrow, and earn interest on crypto assets. No bank or middleman sits between them.

The name comes from a Latin term for a consumable loan. The project says this reflects its lending focus. Mutuum runs on Ethereum and uses smart contracts to automate the entire loan process.

Tokenomics of Project

MUTM has a fixed total supply of 4,000,000,000 tokens. The official allocation from Mutuum's documentation is below.

Allocation

Percentage

Tokens

Presale

45.5%

1,820,000,000

Liquidity Mining and Incentives

10%

400,000,000

Ecosystem Growth and Developer Rewards

10%

400,000,000

Security and Shortfall Reserve

10%

400,000,000

Liquidity

10%

400,000,000

Partnerships

5%

200,000,000

Community Incentives and Giveaways

5%

200,000,000

Team and Founders

4.5%

180,000,000

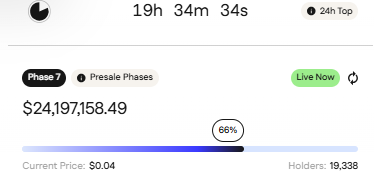

As of the latest official updates, the Mutuum Finance presale sits in Phase 7 of 11. The price is $0.04 per token.

Phase 1 opened at $0.01. These figures change often, so this review will update them as new milestones are posted.

Technology Behind MUTM

Mutuum Finance is built as an ERC-20 protocol on Ethereum. The team has stated plans to expand to other chains later. No confirmed timeline for that expansion exists yet.

Security work includes a completed audit from Halborn Security.

The project also reports a CertiK Token Scan score of 90 out of 100. A live $50,000 bug bounty program adds another layer of review.

Mutuum Finance Latest Update: July 2026 Presale is live.

Source: official website mutuum.com

The Mutuum finance presale remains active in Phase 7, priced at $0.04 per token. Phase 8 is expected to raise the price to $0.045.

More than $24.19 million has been raised from over 19,338 holders.

The project has continued to tie funding milestones to development progress rather than treating them as standalone numbers.

Recent updates on its official X account have linked new raise figures to planned feature releases for the V1 protocol, alongside stated plans for Layer-2 scaling integration and a native, over-collateralized stablecoin in later development stages.

Important Note:Mutuum Finance Presale figures and phase tiers move rapidly. Investors must always confirm the active phase and live token price directly on the official portal before committing any funds.

Presale Vesting Schedule of Mutuum Finance

Mutuum Finance tokens unlock on a fixed six-month schedule. Nothing unlocks in month one; that's the cliff. From month two onward, tokens release in equal steps until the full amount is available.

Month

Unlocked

Month 0 (TGE)

0%

End of Month 1

0% (Cliff)

End of Month 2

20%

End of Month 3

40%

End of Month 4

60%

End of Month 5

80%

End of Month 6

100%

This structure means Mutuum Finance presale buyers cannot sell immediately after listing. That lowers the risk of an early sell-off hitting the token price.

Team and founder tokens carry a longer, 18-month schedule with a six-month cliff, followed by linear monthly unlocks.

How Does Mutuum Finance Work

The protocol runs two lending markets side by side.

Peer-to-Contract (P2C): Lenders deposit assets like ETH or USDT into a shared pool. Borrowers draw from that pool using secured crypto loan positions. Interest rates adjust automatically based on pool usage.

Peer-to-Peer (P2P): Two users agree on custom loan terms directly. The project says this model suits non-standard or higher-risk assets. These would not fit safely into a shared pool.

Risk Comparison: P2C vs P2P Lending

Lending Model

Where the Risk Lies

Core Dangers

How It Is Managed

Peer-to-Contract (P2C)

Shared Systemic Risk: Your crypto goes into a massive shared pool. If the main contract breaks, everyone loses together.

Hackers finding a bug in the shared pool code.

The platform uses automatic interest adjustments and backup emergency funds to protect the pool.

Peer-to-Peer (P2P)

Private Counterparty Risk: Your loan is a direct deal with one person. If they default, the loss is yours alone.

The specific borrower failed to pay you back.

You set custom terms, demand extra collateral from the borrower, and choose exactly who you trust.

Core Architecture & Key Features

The core system includes liquidity pools, collateral contracts, and a liquidation process. Smart contracts track every deposit, loan, and collateral ratio in real time. If collateral value drops too far, liquidation protects the pool.

According to Mutuum Finance Presale, its V1 architecture has been deployed to Ethereum's Sepolia testnet. Reported test assets include ETH, USDT, LINK, and WBTC. More assets are planned after mainnet launch.

mtTokens: Suppliers to a P2C pool receive mtTokens in return. These represent the deposit plus accrued interest, and they are transferable.

Debt Tokens: Borrowers get tokens that track their outstanding balance. This makes obligations easy to monitor on-chain.

Variable and Stable Rates: Users can pick rates that shift with pool demand. Fixed rates are also available for predictable planning.

Liquidator Function: Anyone can liquidate an undercollateralized loan. This open role helps keep the protocol solvent.

Non-Custodial Design: Users keep ownership of their assets throughout. The platform never takes custody of deposits.

Roadmap & Token Utility

The roadmap runs across several stages. These include early development, security review, testnet deployment, and mainnet launch. The team completed a Halborn security audit and deployed V1 to the Sepolia testnet.

A native, over-collateralized stablecoin is listed as a later-stage goal. Layer-2 scaling integration is also on the roadmap. No confirmed mainnet launch date has been announced through official channels yet.

MUTM is the protocol's native token. According to the project, it supports platform incentives and liquidity mining rewards. It is also positioned for future governance participation.

Protocol revenue is intended to fund token buybacks over time. The project says this approach supports demand without increasing total supply.

Advantages

Dual lending markets (P2C and P2P) suit different asset types.

A non-custodial structure keeps funds under user control.

Independent audit from Halborn, plus a public CertiK score.

An active bug bounty adds extra scrutiny on the code.

Published tokenomics with clear, official vesting schedules.

Challenges and Risks

The core team has not been named publicly. This is a transparency gap worth noting.

No mainnet date has been confirmed. The protocol remains unproven outside testnet.

Mutuum Finance Presale tokens stay illiquid until the vesting schedule releases them.

Several unofficial sites mimic the Mutuum brand in search results.

Mutuum's own X account has warned it runs no support account. It says it will never message users first, which points to active impersonation attempts.

Vision of Mutuum Finance

Mutuum Finance frames its mission simply: replace bank-style lending with something transparent and rules-based. No loan officer, no hidden fee schedule. Smart contracts run the whole cycle: deposits, loans, interest and liquidations, nobody sits in the middle taking a cut.

Longer term, the project is aiming past a single chain. Its stated goal is a multi-chain lending network built to serve everyday users and institutions side by side, not one or the other.

Where does that ambition come from? The team points to two recurring problems in DeFi lending: not enough asset variety and loan terms that don't flex. Their answer is running two markets instead of one. A blue-chip token and a thinly traded altcoin don't carry the same risk, so Mutuum treats them differently; each market gets its own rules, its own risk profile, and its own protections.

How to Buy and Where to Buy Mutuum Finance Tokens: Step by Step

Buying into the presale means working through the official site, start to finish. Nothing about the process is optional or skippable.

Head to the official website,mutuum.com. Double-check the domain before you connect anything; this step catches most scam attempts before they start.

Get a Web3 wallet set up. MetaMask and Trust Wallet both handle ERC-20 tokens without issue.

Fund it. ETH, USDT, USDC, BNB, and MATIC are all supported.

Hit "Connect Wallet" on the presale dashboard.

Type in how much MUTM you want and confirm.

Your MUTM balance shows up on the dashboard right after.

Note:MUTM is not yet listed on any exchange at present. Any offer to buy it elsewhere should be treated as a scam.

Future Outlook and Final Thoughts

The next major milestones are a confirmed mainnet date and the final Mutuum Finance presale phases. Real performance will depend on user deposits and borrowing volume after launch. It also depends on whether the stablecoin and multi-chain plans ship on schedule.

This review shows a project with published tokenomics and a working testnet. Independent audits add a layer of transparency.

Real early-stage risk remains too, including an unnamed team and no confirmed mainnet date. Readers should treat presale participation as high-risk and verify every detail on mutuum.com directly.

Expert Opinion

Structured presales with public vesting and third-party audits often signal a more disciplined process. Mutuum Finance published audit results and bug bounty programme support that read.

At the same time, an unnamed team and an open mainnet date are common early-stage risk markers. They are not unique to this project; the same gaps show up across most early-stage DeFi presales.

Disclaimer: This article is for educational and informational purposes only and should not be considered financial or investment advice. Always conduct your own research before making investment decisions.