The result was a market that looked weak on the surface but remained structurally healthier than many previous corrections.

A

AnonymousCryptoCompass newsroom

June 28, 2026

8 min read

ANALYSIS

CryptoCompass editorial visual for markets coverage.

Executive Summary

If one theme defined the final full week of June, it was risk repricing.

Crypto investors spent the week navigating an increasingly complicated macro environment. Military tensions between the United States and Iran pushed oil markets back into focus. Shipping risks around the Strait of Hormuz reminded investors that geopolitical shocks can quickly spill into inflation expectations and central bank policy.

Yet despite those headwinds, Bitcoin once again demonstrated why it is increasingly viewed differently from the rest of the digital asset market.

Altcoins broadly declined.

Speculative sectors suffered heavy losses.

Institutional adoption continued quietly accelerating.

Infrastructure continued expanding.

Regulation continued moving forward.

The result was a market that looked weak on the surface but remained structurally healthier than many previous corrections.

Perhaps the most important lesson from the week is this:

Price action and fundamental progress are increasingly moving at different speeds.

A Market Trading Headlines Instead Of Narratives

For much of 2025, crypto traded around optimism.

ETF inflows.

Stablecoins.

Institutional adoption.

Artificial intelligence.

Tokenization.

This week, however, markets returned to something much older.

Geopolitics.

Following renewed military operations involving the United States and Iran, investors immediately began reassessing energy markets, shipping risks and inflation.

The Strait of Hormuz once again became one of the most closely watched locations in global finance.

Roughly one-fifth of the world's seaborne oil passes through this narrow corridor.

Even the possibility of disruption is enough to move commodities, insurance premiums and market sentiment.

For crypto, the implications extend beyond oil.

Higher energy prices could delay future rate cuts.

Persistent inflation could keep monetary policy restrictive.

Risk assets would likely remain under pressure.

Bitcoin therefore spent much of the week caught between two competing narratives.

Higher geopolitical uncertainty supports demand for alternative stores of value.

Higher interest rates reduce liquidity across speculative markets.

Those two forces largely offset each other.

Bitcoin Once Again Outperformed The Broader Market

While headlines focused on falling prices, market structure told a more nuanced story.

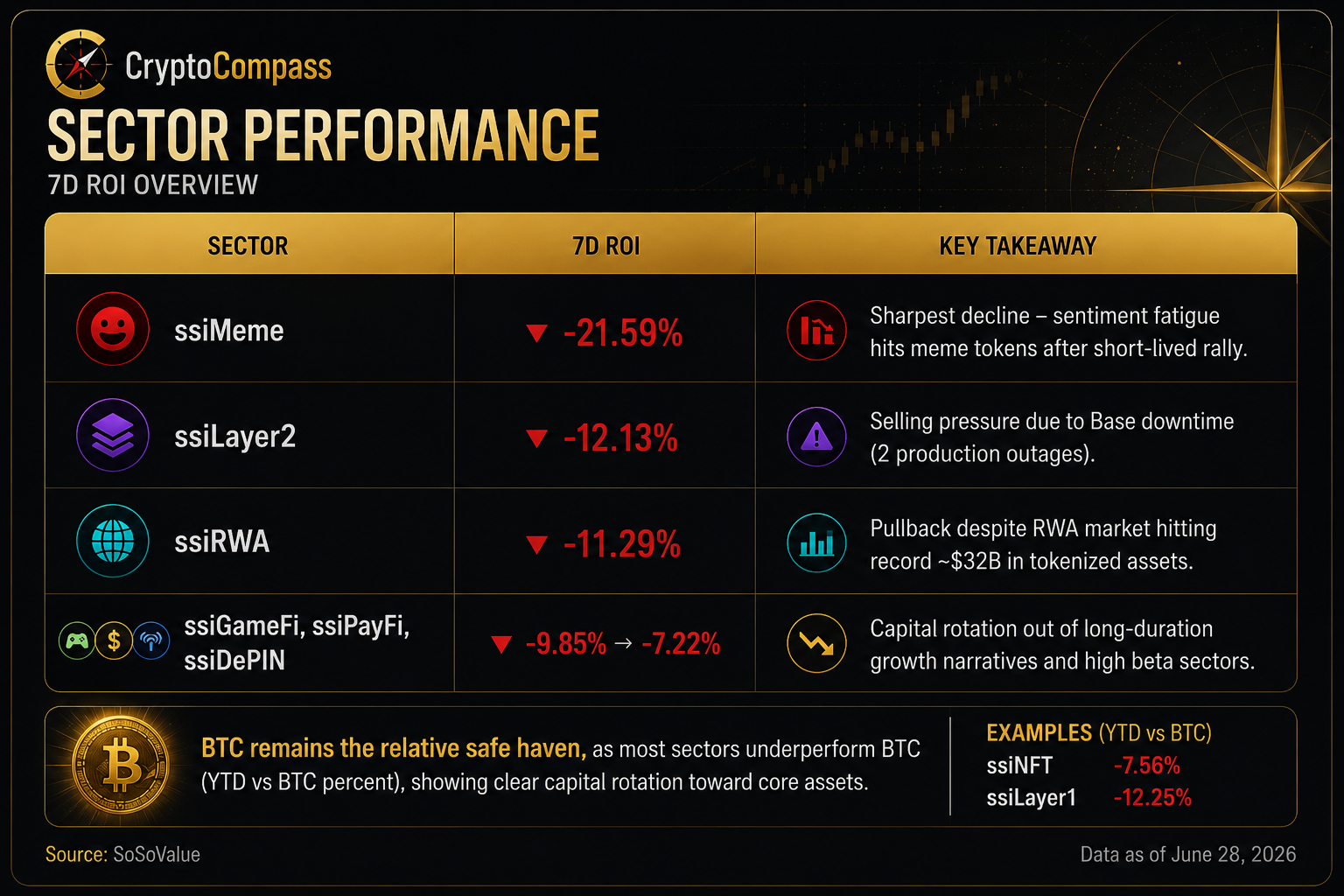

According to SoSoValue sector indices, every major crypto sector finished the week lower.

The largest declines occurred across speculative segments.

Meme Coins

Down more than 21%.

The sector that led much of the previous speculative rally became the week's weakest performer.

Layer 2

Declined over 12%.

Beyond macro pressure, confidence was affected by operational concerns after Base experienced multiple production interruptions.

Real World Assets (RWA)

Lost more than 11%.

Interestingly, this occurred despite continued growth in tokenized asset issuance.

Fundamentals improved.

Token prices declined.

This divergence suggests investors were reducing risk broadly rather than reacting specifically to RWA fundamentals.

GameFi, PayFi and DePIN also recorded notable losses as capital rotated toward larger and more liquid assets.

Bitcoin once again became the market's defensive position.

That is an increasingly familiar pattern.

When investors reduce exposure, they are no longer leaving crypto entirely.

They are moving toward Bitcoin.

That behavioural change reflects a more mature market than previous cycles.

Liquidity Remains The Market's Strongest Foundation

One of the easiest mistakes investors make during corrections is confusing falling prices with disappearing liquidity.

Those are not always the same thing.

ETF flows slowed during the week but remained substantially healthier than earlier in the month.

Stablecoin supply continued holding near record levels.

Tokenized asset issuance continued expanding.

Exchange infrastructure continued improving.

Institutional custody services continued growing.

Taken together, these indicators suggest that liquidity has not left the ecosystem.

It has simply become more selective.

That distinction matters.

Bull markets rarely end because infrastructure disappears.

They usually pause because investors become cautious.

Liquidity often returns long before sentiment does.

Institutions Continue Accumulating Bitcoin

Away from daily price movements, institutional adoption continued strengthening.

According to Fidelity Digital Assets, the number of publicly listed companies holding at least 1,000 Bitcoin has expanded dramatically over the past eighteen months.

Collectively, corporate treasuries now control roughly six percent of Bitcoin's maximum supply.

That statistic deserves more attention than it received.

For years, Bitcoin was viewed primarily as a speculative asset.

Increasingly, corporations are treating it as a treasury reserve.

Every new corporate buyer slightly reduces future circulating supply.

Unlike retail speculation, treasury allocation tends to operate on multi-year investment horizons.

That changes the supply dynamics of the entire market.

Meanwhile, ARK Invest continued increasing exposure across digital asset infrastructure through investments linked to Coinbase, Circle and other blockchain-related businesses.

These are not short-term trading decisions.

They represent long-term positioning around the financial infrastructure being built underneath crypto.

Tokenization Continues Expanding Quietly

One of the week's most overlooked themes was the continued growth of tokenized real-world assets.

Although RWA-related tokens declined alongside the broader market, the underlying infrastructure continued expanding.

Private credit products.

Institutional lending.

On-chain collateral.

Tokenized securities.

These developments rarely generate the excitement of meme coins.

But they may ultimately prove far more important.

Every new institutional product built on blockchain expands the addressable market for digital assets.

Crypto's future will likely be determined less by speculative trading and more by financial infrastructure.

That transition continues almost every week.

Regardless of short-term prices.

Regulation Continues Moving Toward Integration

Governments also continued redefining their relationship with digital assets.

Rather than asking whether crypto should exist, policymakers are increasingly asking how it should integrate into existing financial systems.

Stablecoin legislation continued advancing in Washington.

Central banks expanded discussions around systemic crypto risks.

Multiple jurisdictions continued developing licensing frameworks for institutional participation.

This represents a significant change compared to previous cycles.

Regulation is gradually shifting from prohibition toward integration.

That evolution may ultimately become one of the industry's strongest long-term catalysts.

Speculation Never Truly Disappears

Despite broad market weakness, crypto once again demonstrated its unique ability to generate extraordinary speculation.

The surprise story of the week came from ANSEM-related meme tokens.

Within hours, some traders reported returns exceeding one hundred times their original investment.

For many observers, this appeared irrational.

In reality, it reflected something more fundamental.

Speculation is not disappearing.

It is becoming increasingly concentrated.

As overall liquidity tightens, capital searches aggressively for narratives capable of producing asymmetric returns.

The opportunities become fewer.

The volatility becomes greater.

The risks increase accordingly.

Episodes like ANSEM are reminders that crypto remains a market driven as much by psychology as by valuation.

Macro Risks Still Dominate The Outlook

Several macro developments continue demanding close attention.

Markets remain focused on:

• Middle East stability.

• Oil prices.

• Federal Reserve policy.

• Inflation data.

• Treasury yields.

• The U.S. dollar.

These variables increasingly influence crypto just as much as blockchain-specific news.

That is one of the defining characteristics of the current cycle.

Crypto is no longer trading in isolation.

It is trading as part of the global macro system.

CryptoCompass View

This week looked disappointing if viewed only through prices.

It looked encouraging if viewed through infrastructure.

Bitcoin adoption continued.

Institutional participation expanded.

Stablecoin regulation progressed.

Tokenization advanced.

Corporate treasury allocation accelerated.

Infrastructure kept improving.

Meanwhile, Bitcoin continued demonstrating relative resilience while speculative sectors absorbed the majority of market stress.

That divergence tells an important story.

The crypto market is changing.

The speculative layer remains volatile.

The foundational layer continues strengthening.

Long-term investors should pay close attention to the latter.

History suggests infrastructure is built during periods of uncertainty.

Every investor in crypto eventually asks the same quiet question: where does the real money actually get made? The search for the best crypto presale to buy in July 2026 keeps circling back t

General Motors will launch its own in-vehicle artificial intelligence assistant later this year, designed to reach further into the car than the Google Gemini system it started deploying in t

BitcoinWorld Strategy Keeps August Dividend Rate for STRC Preferred Stock at 12% Strategy (formerly MicroStrategy) has confirmed that the August Stretch Dividend Rate for its STRC preferred s