How Not to Lose Money on Sketchy Sites: My Experience with Two Cards

BTC

Online shopping always seemed easy and painless — until you open your bank statement one day and realize: the money’s gone, and there’s no support in sight. Sound familiar? I’ve seen it a million times — my neighbor nearly lost her entire paycheck on a “too-good-to-be-true” site, my brother typed in the wrong address and handed his cash straight to scammers, and a friend spent six months trying to get a couple hundred bucks back from a subscription that kept charging him every month.

This isn’t about “stupid people.” It’s about ordinary people with ordinary money trusting the internet. Every time someone says, “It’s safe, don’t worry,” a thousand little stories pop into my head: someone typed their card number too quickly and someone simply didn’t know how the protection mechanisms worked.

This is that familiar pain we’ve all felt at least once — the moment your money leaves your account and your sense of control disappears. And it’s for exactly these moments that I built a system that minimizes losses and keeps you calm.

How to Minimize Risks: Limits, Freezes, and Cold Logic

Most people think protecting online payments is all about vigilance and intuition. Funny, right? In practice, vigilance without a system is like holding a Swiss Army knife and trying to cut concrete: sure, you have a tool, but zero results.

Rule #1: Limits — your insurance for nerves and wallet

Don’t keep everything on one card. This isn’t paranoia; it’s common sense. I only keep the amount I can comfortably lose. For example, if you want to try a new site with a rare NFT collection, only load a strictly limited amount onto that card. That way, if “something goes wrong,” it’s unpleasant, but not catastrophic. The formula is simple: available funds = what won’t ruin your mood if lost. Your brain stays calmer, and you learn to treat experiments like a test run, not a high-stakes gamble.

Rule #2: Instant freezes on suspicious transactions

Don’t wait until “tomorrow.” Any weird transaction — react immediately. Pro tip: enable notifications to see every charge attempt in real time. When your card alerts you and you freeze it instantly, it’s like planting a red flag on the front lines before the enemy even breaches your defense. Even if it’s just a system glitch, you’ve bought time and retained control.

Rule #3: Structured risk separation

Money of different trust levels shouldn’t mix with experimental spending. Example: you spot a “too-good-to-be-true” subscription on a brand-new service. Instead of entering your main card details, you use a risk-zone card with a pre-set limit. If it turns out to be a scam — annoying, yes, but you haven’t lost everything.

How I Use Two Cards for Shopping on Sketchy Sites

First, a little context: I don’t divide my cards into “everyday” and “fun.” I divide them by risk level, and that fundamentally changes the way I handle money.

Card 1 — The Safe Zone

This card is my foundation. Money here is for anything tried-and-true, where I’m confident there won’t be surprises. But even here, I don’t keep an endless balance. I think in budgets:

• Everyday expenses — one range

• Subscriptions and services — another

• Bigger payments (like tech or services over $1,000) — separate planning, separate limit

Card 2 — the Experiment Zone

This card is my “playground.” Any new site, unknown service, or subscription with a questionable reputation goes through it. Here’s the key: I never keep large sums on this card. Usually $50–$150 for a test purchase, sometimes a bit more if needed — but always tied to a specific task. This card isn’t for storing money; it’s for testing risk without turning it into a disaster.

How To Use Card 2 Safely?

1. Reloading and Limits

Money only goes in for a specific purpose. Need to pay? Load the exact amount, make the payment, and the card goes back to nearly zero. This removes the possibility of a major loss.

2. Instant Control

All notifications are on. I see every transaction immediately. If something looks off, I freeze the card faster than you can even reach support. In these situations, speed beats analysis.

3. Testing New Services

Every new site goes through this card, even if it looks perfect. Especially if it looks perfect — the first payment is always a test, not a sign of trust.

4. Risk Separation

Card #1 and Card #2 never mix. Ever. Money from the “safe zone” doesn’t flow into the “experiment zone.” It’s like isolation: if something breaks in one system, the other keeps running smoothly.

Top 3 Crypto Cards: 6 Cashback Categories, Bitcoin Investment

When people switch from a bank card to a crypto card, they usually don’t overthink it. If it’s crypto — good enough. But after spending some time in crypto, you start noticing the differences in those cards. And suddenly, choosing a crypto card becomes just as important as choosing an exchange. So, here are three crypto cards that stand out right now for me:

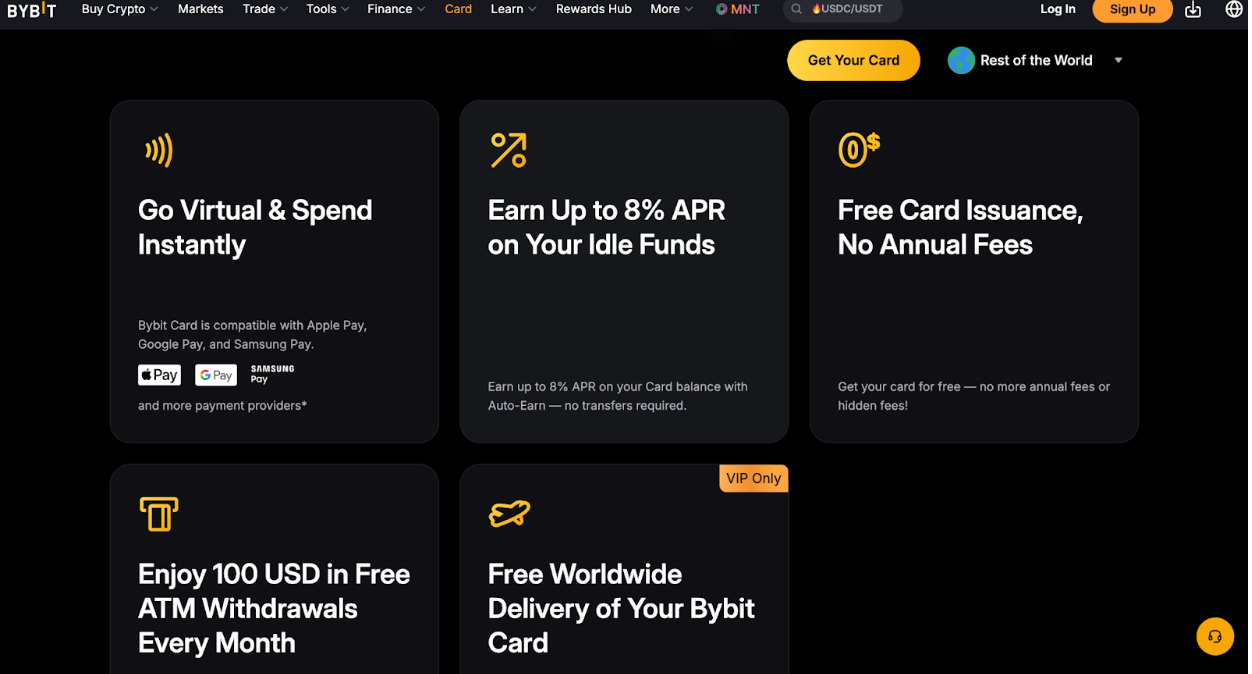

1. Bybit Card

I don’t use this one daily, but it’s a good recommendation if you want one card that does a bit of everything. You can pay with crypto or fiat, earn 2–10% cashback, and even get APR on idle funds — which is something you don’t see often in regular cards. There are also ATM withdrawals, virtual cards, and no annual fees.

It’s the kind of card you keep in mind when you want flexibility without juggling too many tools.

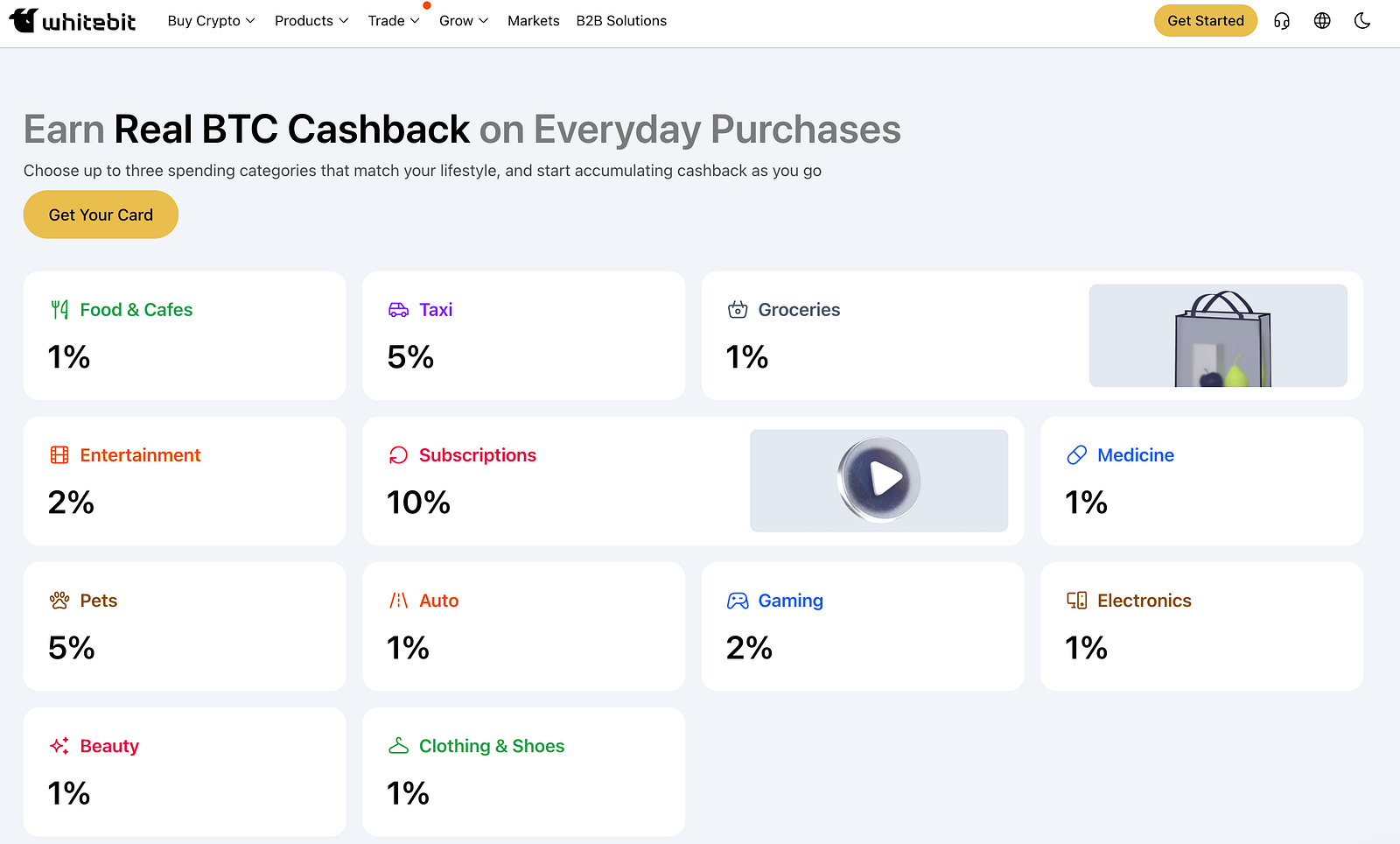

2. WhiteBIT Nova Card

This is the one I use most often. Not because it’s “better,” but because it’s predictable. You pick up to three cashback categories — and if you’re like me and using two cards, that’s already six.

For example, I keep food, subscriptions, and transport on one. The second card covers online services, taxis, and random late-night purchases (we all have those). Suddenly, even routine spending starts quietly accumulating BTC or WBT, and cashback begins to feel like a small, steady investment.

3. MEXC Card

This one is useful when you want more control over your crypto while still spending normally.

Up to 4% cashback, on-chain control, and the ability to spend directly from your crypto balance make it feel more flexible than traditional cards.

It’s the kind of card you use when you don’t want to overthink things — just pay, get cashback instantly, and keep moving.