The Real Reason My Trades Were Underperforming (It Wasn’t the Market)

BTC

Manual trading worked fine — until the market started moving faster than I could keep up. I’d see the signal, make the call, hit the button… and by the time the order went through, the price had already slipped, along with my risk/reward math. In volatile moments, those tiny delays stop being “noise” and start quietly bleeding capital. Eventually it became obvious: the strategy wasn’t the issue, execution was. In crypto, it’s not just about being right on direction — it’s about how fast you can actually act on it. That’s what pushed me toward automation via API in a VIP setup, just to close that annoying gap between thought and fill.

When I Realized Milliseconds Matter: Rethinking Execution Infrastructure

Switching to a VIP API wasn’t just a tool upgrade for me — it fundamentally changed how I interact with the market. Unlike a standard API, where requests are processed in a shared queue, the VIP tier provides priority handling, more stable connectivity, and higher rate limits. In practice, this translates into predictability: orders don’t get “lost” during peak load, and the system executes exactly when it matters most. In an environment where milliseconds count, this difference stops being a technical detail and directly impacts results.

This becomes especially noticeable at the latency level. Previously, there was often a gap between signal and execution due to manual actions or infrastructure constraints. With a VIP API, that lag is minimized:

- Orders are sent and filled faster;

- Reducing slippage and improving entry precision;

In effect, you start operating under conditions closer to those of more advanced market participants — where speed is no longer an advantage but a baseline standard.

At the same time, the key shift isn’t just about speed but about control. Automated triggers, predefined execution logic, and the ability to react to specific market conditions without human intervention eliminate the system’s weakest link — decision-making delay. Manual trading is always limited by perception and reaction time, whereas an algorithm executes a strategy strictly according to defined parameters. As a result, the edge shifts from “clicking faster” to “designing better systems” — and that’s what creates sustainable advantage over time.

The $0.35% Spread That Never Reached My PnL (Until I Fixed This)

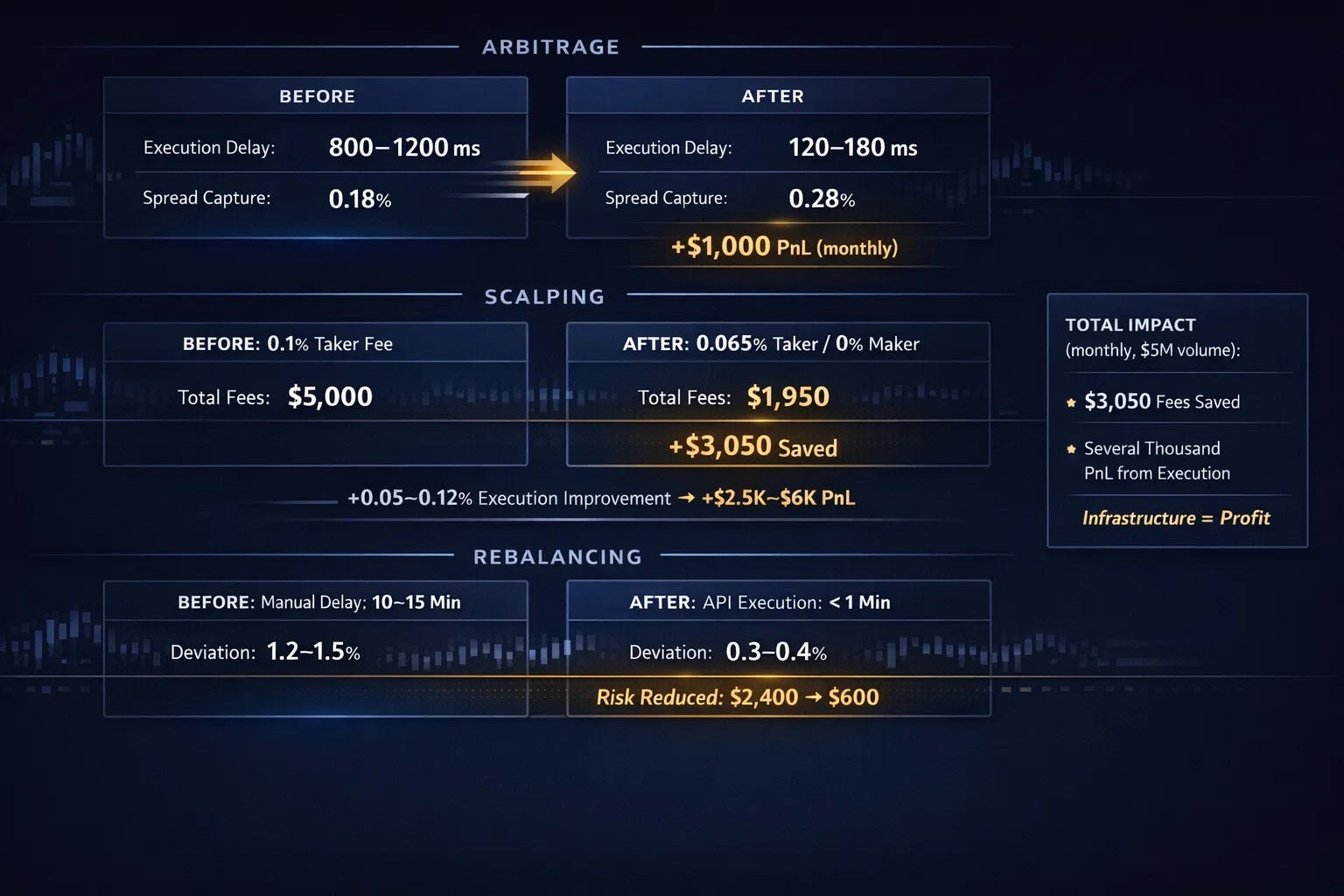

I noticed that the main source of PnL loss in my strategy wasn’t market direction but the order execution infrastructure. After switching to WhiteBIT’s VIP program and connecting the API, I started to view trading as a system: arbitrage, scalping, and portfolio rebalancing as three separate flows with different sensitivities to latency and fees.

In cross-exchange arbitrage, the average execution delay used to be around 800–1200 ms, which meant I was losing a significant portion of the spread. For example, in the BTC/USDT pair, the spread could be 0.35%, but due to slippage, the actual capture dropped to ~0.18%. After switching to an API with priority processing and higher rate limits, execution time decreased to ~120–180 ms, and effective capture increased to ~0.28%. On a $1,000,000 monthly volume, this resulted in roughly $1,000 additional net PnL purely from reduced latency decay.

In scalping, the difference proved even more critical. Before VIP, I mostly operated with taker execution at ~0.1% fees, and with a high number of trades, this significantly ate into margins. After switching to VIP (taker 0.065%, maker 0%) and automating via API, I calculated that at a monthly volume of $5,000,000 (approximately $3,000,000 taker and $2,000,000 maker), trading fees dropped from $5,000 to $1,950. The savings amounted to $3,050 per month without any changes to the strategy itself. Additionally, thanks to faster execution, the average improvement in entry/exit was ~0.05–0.12%, which potentially adds another ~$2,500–$6,000 to PnL depending on volatility.

The most underestimated case is portfolio rebalancing. Previously, I did it manually once a week, and the delay between signal and execution sometimes reached 10–15 minutes. In trending conditions, this created portfolio deviations of ~1.2–1.5%. After switching to API, I reduced this lag to under 1 minute, and the actual deviation dropped to ~0.3–0.4%. In monetary terms, for a $200,000 portfolio, this reduced potential “suboptimal exposure” risk from roughly $2,400 to $600.

Overall, the VIP program for me is not about fee discounts, but about changing the mathematics of the strategy. On a $5,000,000 monthly volume, I effectively gain about $3,050 in fee savings plus several thousand dollars in additional PnL through lower slippage and faster execution. And the key conclusion I’ve drawn is this: in high-frequency and semi-automated strategies, infrastructure directly converts into profit — sometimes even more than market direction itself.

Ultimately,

My own calculations suggest that the shift to a VIP API isn’t some “pro-level secret” — it can realistically add a few extra percent in monthly performance just by cutting slippage, fees, and execution lag, and it’s a lot more straightforward to set up than most traders assume. If you’re curious how these numbers would look in your own setup or want a breakdown of the product, feel free to drop me a DM and I’ll walk you through it.