Web Traffic of Cryptocurrency Exchanges – April 2026

CCY

CCY

UTED

UTED

2026

2026

TOP

TOP

APRIL

APRIL

April 2026 web-traffic for centralized cryptocurrency exchanges (CEXs) paints a clear picture of a highly stratified yet globally interconnected market, where a small group of exchanges captures most user attention while a long tail of platforms competes through regional focus and differentiated offerings. Binance stands out as the leading global hub, while OKX, Coinbase, KuCoin, and a fast-rising cluster of emerging-market platforms such as BingX and LBank continue to compete for user mindshare.

At the same time, the report highlights the persistent divide between globally diversified exchanges and hyper-localized platforms such as Upbit, Bithumb, and CoinDCX, where traffic is overwhelmingly concentrated in a single country. This structural split underscores how regulatory regimes, fiat on-ramp infrastructure, and local trust continue to shape user behavior more than purely global branding.

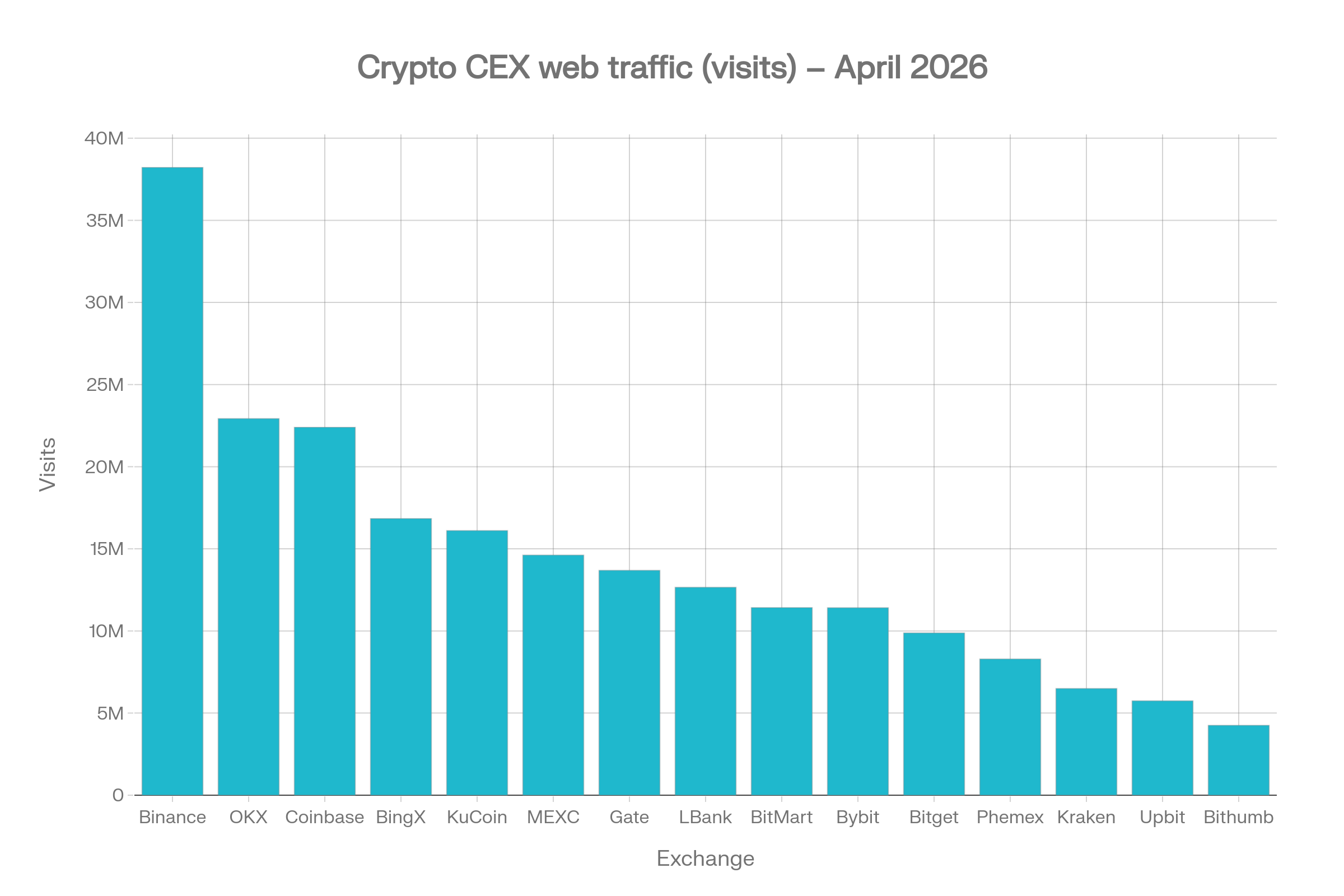

Top exchanges by April 2026 web traffic

Top 10 by latest monthly visits

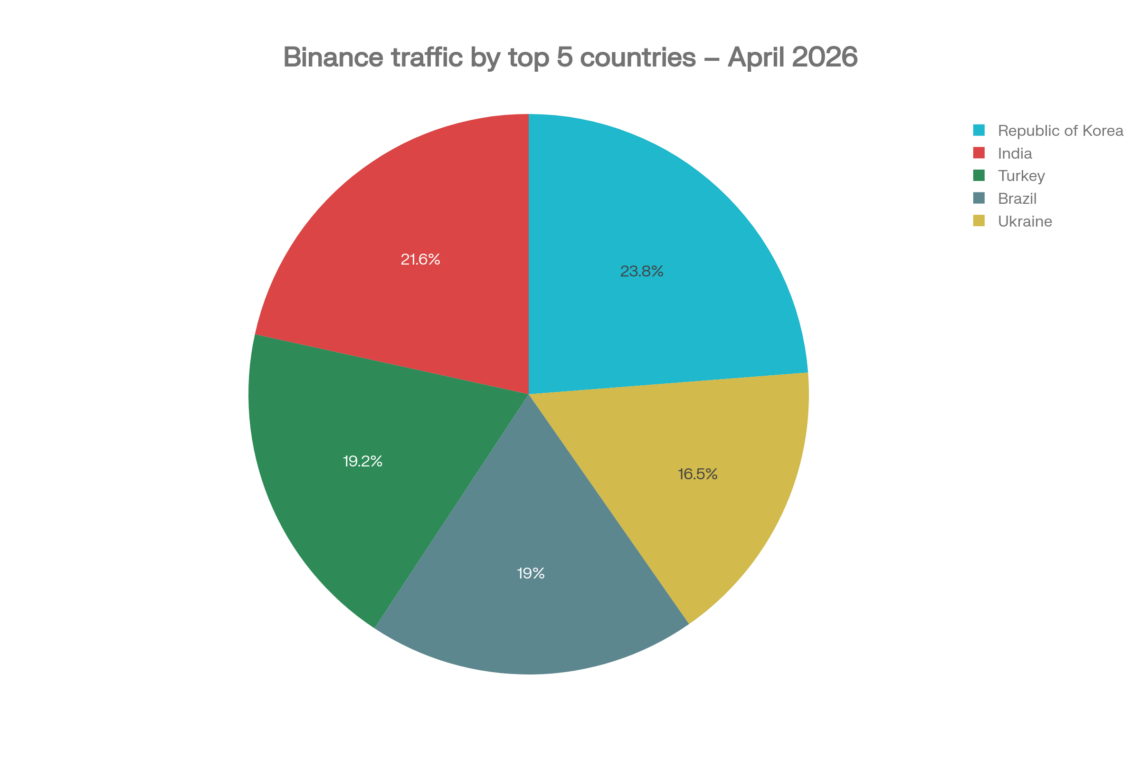

- Binance: Binance leads with approximately 38.22 million monthly visits, maintaining a clear advantage at the top of the market. Its traffic is globally diversified across the Republic of Korea (7.79%), India (7.07%), Turkey (6.28%), Brazil (6.22%), and Ukraine (5.42%), with no single country dominating usage. This distribution reinforces Binance’s position as the default global CEX for a broad retail user base.

- OKX: OKX follows closely among tier‑one exchanges with about 22.93 million visits. Its top markets include Brazil (6.82%), Turkey (6.39%), Japan (6.37%), the United States (6.17%), and Vietnam (5.68%), signalling a balanced presence across the Americas and Asia rather than heavy reliance on any single jurisdiction.

- Coinbase: Coinbase recorded roughly 22.40 million visits, solidifying its status as the leading regulated U.S. exchange. Its traffic is heavily concentrated in the United States (69.68%), with smaller shares from the United Kingdom (5.05%), Germany (2.50%), Canada (2.25%), and France (2.19%), underscoring its Western and U.S.‑centric footprint.

- BingX: BingX generated approximately 16.84 million visits, putting it into the upper tier despite being a relatively newer derivatives‑focused platform. It has a strongly emerging‑market skew, with key contributions from Turkey (18.31%), Australia (14.39%), Argentina (12.77%), Kazakhstan (7.77%), and Ukraine (4.20%), highlighting its appeal in regions facing currency volatility and capital controls.

- KuCoin: KuCoin logged around 16.11 million visits, supported by a diversified audience across the United States (7.39%), the Philippines (6.95%), Singapore (5.06%), India (4.48%), and Azerbaijan (4.34%). This mix aligns with its positioning as a global altcoin and retail‑trader hub.

- MEXC: MEXC saw about 14.62 million visits, cementing it as a major challenger in the derivatives and altcoin listing segment. Its traffic is heavily driven by Vietnam (18.14%) and Algeria (10.64%), along with notable contributions from India, Japan, and Pakistan, signaling a deep focus on emerging markets.

- Gate: Gate.io recorded roughly 13.69 million visits, powered by a diverse mix of users from the United States (13.04%), the Republic of Korea (6.33%), the Philippines (4.53%), Vietnam (3.64%), and Turkey (3.44%). This balanced distribution reflects its strategy of catering to altcoin traders across multiple regions.

- LBank: LBank attracted about 12.66 million visits, with a strong footprint in the Philippines (10.13%), Azerbaijan (7.03%), the United States (5.28%), Senegal (4.60%), and the Republic of Korea (4.13%). Its profile is distinctively emerging‑market heavy but more globally distributed than single‑country specialists.

- BitMart: BitMart reached approximately 11.42 million visits, drawing traffic from the United States (14.51%), the Philippines (7.00%), Turkey (5.45%), Taiwan (5.25%), and the Republic of Korea (5.10%). This mix underscores its role as a global retail gateway, particularly in Asia and North America.

- Bybit: Bybit logged around 11.41 million visits with a strong concentration in Russia (32.14%), followed by the Republic of Korea (8.93%), Ukraine (6.00%), Turkey (2.97%), and Belarus (2.86%). Its user base is skewed toward derivatives traders in Eastern Europe and Asia.

Momentum across mid‑tier and niche exchanges

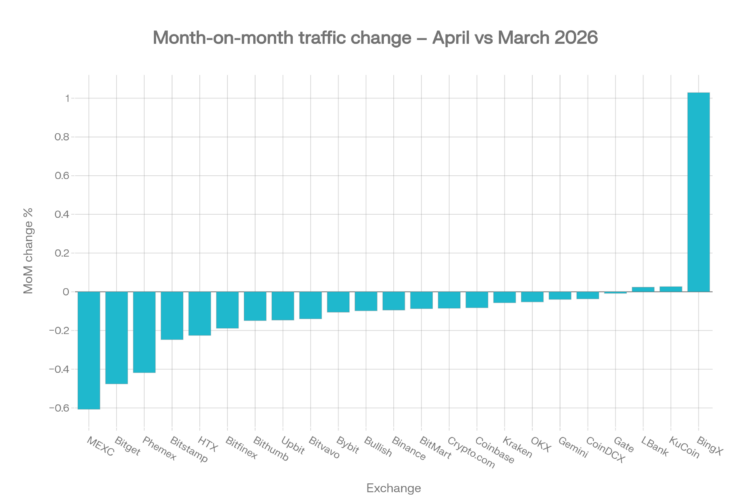

While the leaderboard highlights absolute scale, April 2026 also reveals significant divergence in momentum across mid‑tier platforms, as captured by MoM traffic changes.

Most exchanges experienced negative MoM traffic, consistent with a cooling or normalization phase after earlier spikes in speculative activity. Binance (−9.47%), Coinbase (−8.26%), Bybit (−10.53%), MEXC (−60.71%), Bitget (−47.60%), and Phemex (−41.78%) all saw sizable declines, especially among derivatives-heavy venues where trader engagement is more cyclical. Similar traffic normalization trends were already becoming visible during CEX Web Traffic in March 2026, suggesting that April extended a broader market consolidation phase rather than marking a sharp reversal in user activity.

In contrast, only a few exchanges posted positive MoM growth: KuCoin (+2.65%), LBank (+2.39%), and most notably BingX with a dramatic +102.91% increase, effectively more than doubling its monthly traffic versus the prior baseline. This surge likely reflects aggressive marketing, copy‑trading campaigns, or increased derivatives demand in its core regions.

- Kraken sits in the mid‑tier with several million visits and a Western‑heavy user base led by the United States, the United Kingdom, Canada, France, and Germany, positioning it as an advanced trading and staking venue for regulated users.

- Upbit and Bithumb each record multi‑million visits but are almost entirely Korean in origin (over 97% of traffic from the Republic of Korea), making them dominant domestic exchanges with limited international reach.

- Crypto.com, Gemini, CoinDCX, Bitvavo, Bitstamp, Bitfinex, and Bullish represent smaller yet strategically important platforms, each serving focused regional or institutional niches.

Regional patterns and country‑level concentration

April 2026 web traffic reveals four structural archetypes that define how exchanges position themselves geographically. This geographic segmentation also mirrors trends observed in CEX Web Traffic in Q1 2026, where exchanges with diversified international user bases generally showed greater resilience, while regionally concentrated platforms remained heavily dependent on domestic regulatory conditions and local investor sentiment.

Korea‑centric exchanges

Upbit and Bithumb remain the clearest examples of hyper‑localized platforms, with nearly all traffic stemming from South Korea. Upbit draws about 97.17% of its visits from the Republic of Korea, while Bithumb’s Korean share is around 98.21%, with only marginal traffic from the United States, Vietnam, Indonesia, and Turkey.

This extreme domestic concentration underscores strong brand trust, regulatory alignment, and deep fiat connectivity in a single market, but it also concentrates risk: regulatory changes, taxation shifts, or macro shocks in Korea can significantly impact both platforms simultaneously.

U.S.‑anchored, regulated venues

Coinbase, Kraken, Gemini, and Crypto.com lean heavily on the United States and other Western markets. Coinbase is the most concentrated, with nearly 70% of traffic coming from the U.S., while Crypto.com also has close to half of its visits from American users, complemented by the United Kingdom, Canada, Germany, and France.

Kraken and Gemini show slightly more European diversification, but still rely on Western jurisdictions where regulatory frameworks are relatively mature and institutional adoption is higher. These platforms benefit from compliance credibility and fiat on‑ramp strength but have slower penetration in emerging markets compared with more aggressive competitors.

Emerging‑market specialists

Several platforms focus on high‑growth, higher‑volatility regions:

- MEXC is heavily skewed toward Vietnam (18.14%) and Algeria (10.64%), along with India, Japan, and Pakistan, indicating a strategy centered on markets where traditional financial access may be limited.

- Bybit depends strongly on Russia (32.14%) and has meaningful traffic from South Korea, Ukraine, Turkey, and Belarus, reinforcing its profile as a derivatives venue popular in Eastern Europe and parts of Asia.

- CoinDCX is overwhelmingly India‑first, with around 78.56% of its visits from India, reflecting its focus on domestic retail onboarding.

These specialization plays can achieve scale quickly but introduce exposure to geopolitical and regulatory shocks in a single or small set of countries.

Globally diversified platforms

Binance, OKX, KuCoin, Gate, Bitget, LBank, and BitMart exhibit the most balanced geographic distribution, drawing users from multiple continents without overreliance on any one market.

Binance, for example, has mid‑single‑digit traffic shares from South Korea, India, Turkey, Brazil, and Ukraine, while OKX blends users from the United States, Brazil, Japan, Vietnam, and Turkey. KuCoin, Gate, Bitget, LBank, and BitMart each combine North American, European, and emerging‑market flows, aligning with strategies built around broad product offerings and flexible onboarding paths.

Key insights from April 2026

1. Market leadership is tied to scale and diversification

Binance remains the reference point for global CEX traffic, but its advantage rests not only on raw visit volume, but also on diversified regional demand spanning Asia, Europe, and Latin America. OKX, KuCoin, Gate, Bitget, LBank, and BitMart are following similar multi‑region strategies, seeking resilience against localized shocks.

In contrast, highly concentrated platforms such as Upbit, Bithumb, and CoinDCX show strong domestic dominance but little evidence of global expansion, reinforcing a structure where some exchanges are effectively national champions rather than global players.

2. Emerging markets drive incremental attention

Countries such as India, Brazil, Vietnam, Turkey, Algeria, the Philippines, and various markets in Eastern Europe and Central Asia contribute a disproportionate share of traffic to many fast‑growing exchanges. Platforms like MEXC, Bybit, BingX, Bitget, LBank, and BitMart increasingly act as gateways for users in these regions who may face capital controls, inflation, or limited local investment options.

This pattern aligns with a broader macro narrative in which crypto functions as both a speculative asset class and an alternative financial rail in emerging economies.

3. April shows normalization after earlier spikes

The prevalence of negative MoM changes across major exchanges indicates that April 2026 was more of a consolidation month than a fresh breakout in retail exuberance. Derivatives‑heavy venues like MEXC, Bitget, and Phemex saw the sharpest pullbacks (around −60.71%, −47.60%, and −41.78% respectively), consistent with fading high‑leverage trading after earlier volatility.

However, positive MoM growth at KuCoin, LBank, and especially BingX suggests that user attention is not retreating uniformly; instead, it is rotating toward specific platforms and regions where product offerings and marketing are particularly resonant.

4. Multi‑exchange usage is likely increasing

The coexistence of globally diversified hubs (Binance, OKX, KuCoin) with regionally dominant or niche platforms strongly implies that active traders increasingly maintain accounts across multiple exchanges. Users may rely on one venue for fiat on‑ramp and regulated holdings (for example, Coinbase or Kraken), while turning to others for derivatives, altcoin exposure, or localized liquidity.

This behavior amplifies competition for listing quality, depth of market, and incentive programs, and it is consistent with patterns documented in earlier traffic and token‑listing studies for 2025–2026.

Conclusion

April 2026 confirms that the centralized exchange landscape is evolving into a hybrid global‑regional system, where a handful of platforms dominate cross‑border traffic while others maintain entrenched local control. Binance continues to set the benchmark for both scale and diversification, but challengers such as OKX, KuCoin, MEXC, Bitget, LBank, and BingX are increasingly leveraging emerging markets and specialized products to expand their footprints.

At the same time, Korea‑centric exchanges (Upbit, Bithumb) and India‑focused platforms (CoinDCX) demonstrate that regional champions remain highly relevant wherever regulation, fiat connectivity, and cultural trust coalesce around a domestic brand. For traders, token projects, and institutional participants, exchange web traffic in April 2026 should be read as a high‑signal complement to on‑chain data and volume metrics revealing not only where liquidity resides today, but also where user attention, regional adoption, and competitive pressure are moving next.

References: A downloadable dataset for the Web Traffic of Cryptocurrency Exchanges – April 2026 report is available on GitHub.