Why All-in-One Money Platforms Are Redefining Fintech’s Future

BTC

Fintech today often looks less like a coherent system and more like a construction kit assembled from disconnected parts without a unified architecture. In a typical mid-sized business, the stack can easily include 5–8 providers: one handles payment processing, another custody, a third covers AML, and yet another manages currency conversion. Formally, everything “works,” but the real complexity starts when you look at how these components interact.

It’s precisely these interfaces that almost always turn out to be the most expensive part. This is where integration time is lost, hidden fees emerge that weren’t obvious at the outset, operational risk accumulates, and critical dependence on third-party SLAs builds up. One provider slows down — and the entire chain starts to desynchronize. And then a logical question arises: is this really a system, or just a set of services that have happened to learn how to interact with each other?

Airwallex Changed My View on Fintech Architecture — Here’s Why It Matters

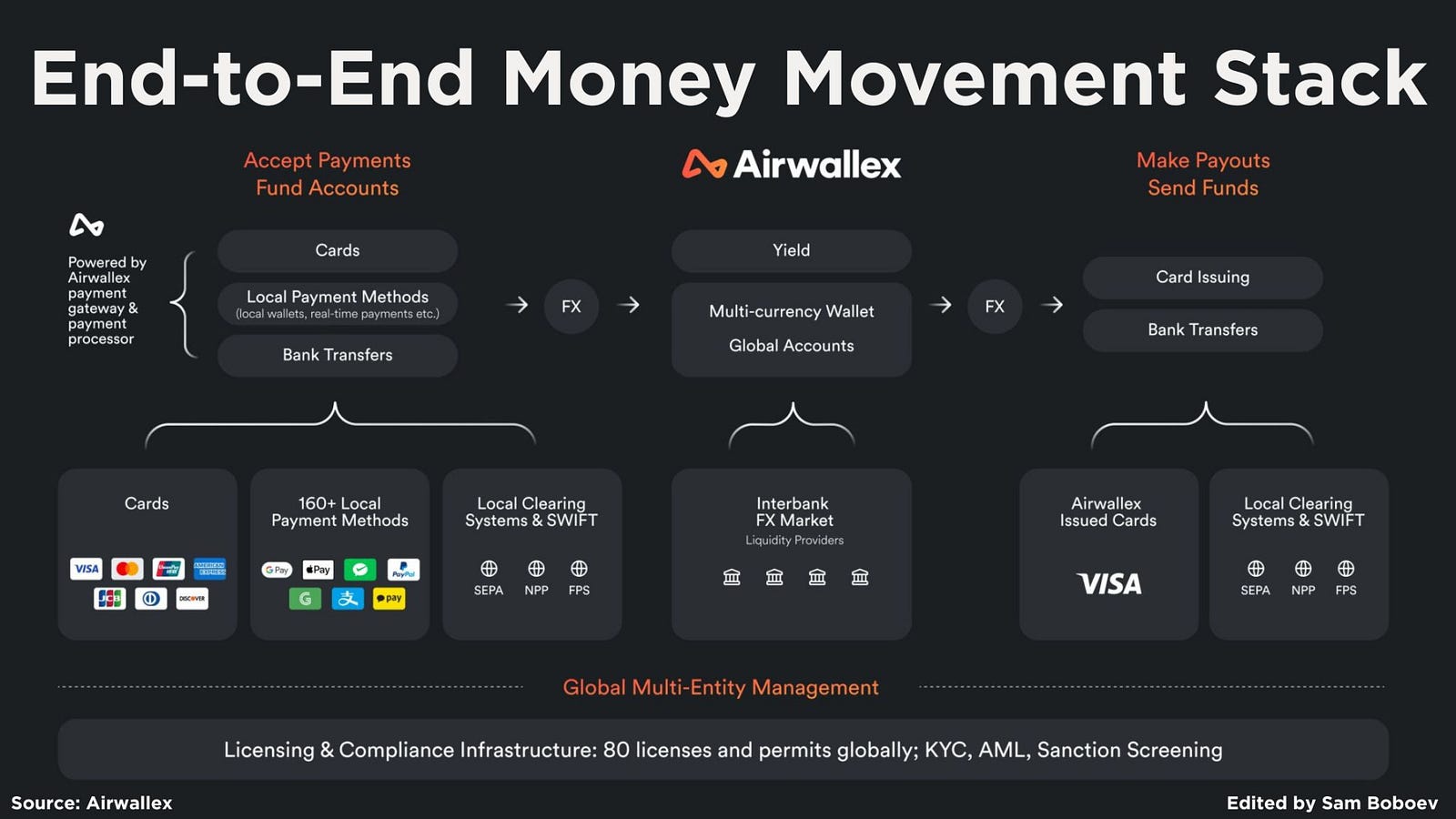

A strong real-world example is Airwallex. The key isn’t just that they “bundled a lot of features together,” but that they built an entire money lifecycle inside a single system where funds effectively never leave the ecosystem. Accept, convert, hold, payout — everything happens within one product without constantly integrating dozens of external providers. On top of that, most payments run through local rails like SEPA or FPS instead of SWIFT, meaning money moves locally, almost like within a unified network. Then there’s the FX layer, where companies can hold multi-currency balances and only convert when it actually makes sense.

Source: Sam Boboev - LinkedIn

From an architectural perspective, it becomes clear why this model scales faster than the traditional point-solution approach. When payments, custody, and FX are split across separate services, you don’t just pay fees at every step — you also lose system connectivity. A platform approach, on the other hand, “stitches” the entire money flow into a single stream where each stage reinforces the next. That’s why you see a compounding effect not only in revenue, but also in valuation — from $1B in 2019 to $5.5B+ in 2023 and beyond. But the more important point isn’t the numbers; it’s the logic: fewer friction points in the financial chain means fewer losses and a more efficient operating model.

Crypto as Core Logic: Rewiring the Monetary Architecture of Your Product

This is exactly where the next layer logically emerges — crypto. But not as an option to “add a wallet,” rather as a fully-fledged second monetary circuit embedded within the same system where fiat already exists. It’s a natural continuation of the same logic: if funds are already circulating within a closed environment, the next step is to enable them to move not only through banking channels but also through crypto infrastructure.

At this point, it’s not so much the feature set that changes but the product logic itself. By leveraging Wallet-as-a-Service/Crypto-as-a-Service, we move beyond “integration thinking”: crypto stops being an external service and becomes part of the internal monetary system, where fiat and crypto are simply different states of the same balance. For the user, this is no longer “converting to crypto,” but a seamless flow of funds within a unified circuit that covers custody, exchange, payments, and liquidity management. Accordingly, on/off-ramps transform from a separate process into an interface element, and the boundary between fiat and crypto gradually disappears at the user experience level — remaining only within infrastructure and compliance.

The least obvious yet most critical effect is control and liquidity. When all flows are concentrated within a single circuit, it becomes possible to manage the movement of funds internally, minimizing dependence on external providers. This reduces friction, shortens delays, and increases resilience. In such a model, crypto ceases to be “just another integration” and instead becomes the second monetary layer of the product — operating continuously, even when the user doesn’t notice it.

What I Look for When I Say “Closed-Loop” Infrastructure

If you look at the market through the lens of a “closed-loop” logic, it quickly becomes clear: not all WaaS/CaaS solutions are equally valuable. Many of them sell more of a sense of having crypto infrastructure than actually delivering it as a cohesive system. In practice, you still end up assembling it from separate modules — which means the same integration points and the same risks, just wrapped differently.

Take WhiteBIT, for example. Here, you can clearly see a bet on an “everything in-house” model: wallets, AML, KYC, custody, support for over 340 assets and more than 80 networks — without the need to connect third-party services. What matters is not even the number of features but the fact that they are already integrated at the system architecture level. The user doesn’t have to figure out how to synchronize custody with compliance checks or how to ensure liquidity — it’s part of the base layer. Given their scale — $3.4T trading volume, $39B market capitalization, 900+ trading pairs — this looks less like an experiment and more like a mature, well-established infrastructure.

WHO TO CONTACT in case you’re looking for integration on WhiteBIT.

Now let’s look at BitGo. Its key strength lies in institutional-grade custody and support for a 1300+ range of assets and 40+ blockchains. At the level of an individual transaction or user, the cycle can indeed appear closed. But a deeper look reveals that BitGo is primarily about storage and security. Other components are often built around this core. In other words, the foundation is strong, but building a full-fledged product ecosystem usually requires additional external layers.

WHO TO CONTACT in case you’re looking for integration on Bitget.

The situation with Coinbase is more nuanced. It’s a powerful platform in terms of UX control and built-in capabilities: on/off-ramps, transfers, exchange, staking — everything seems to be in place. Its scale — $295B in quarterly trading volume, $49.03B market capitalization, 516B assets on the platform — reinforces confidence in liquidity. At the same time, there’s a caveat: it’s an ecosystem where you largely play by their rules. The architecture is convenient and transparent, but not always fully “yours” when it comes to flexibility in building your own financial stack.

WHO TO CONTACT in case you’re looking for integration on Coinbase.

And this is where the key difference emerges. A “closed loop” is not just a list of features. It’s the level of control over the flow of funds within the product: how dependent you are on external integrations, who owns the data and liquidity, and at which points money leaves the system.

And maybe this is the uncomfortable takeaway:

the real competition in fintech is no longer about features but about who owns the flow. The closer you get to a truly closed-loop system, the less you depend on the outside world — and the more your product starts to behave like infrastructure, not just a service. In the end, it’s not about adding crypto or fiat — it’s about deciding where your system actually begins and ends.